Pictet: The problem with passive bond funds

Passive bond funds are becoming popular with investors, particularly the exchange-traded kind. The trouble is, fixed income doesn't lend itself easily to index tracking.

09.04.2018 | 13:56 Uhr

It's difficult to find a duller-sounding investment than the passive bond fund. Nothing there to get the heart racing, you’d think. But the reality is rather different. As a recent report from the Bank for International Settlements (BIS) concludes, funds designed to track a fixed income index – such as exchange-traded vehicles – can in fact be rather risky.

The fundamental problem is that bonds simply don’t lend themselves easily to passive investing. There are several reasons why that’s the case.

The first is that, because the vast majority of bond indices are capitalisation-weighted, passive investors automatically load up on securities issued by the most indebted governments and corporations. That leaves them more exposed to unfavourable changes in a borrower’s creditworthiness than active investors, who can always vote with their feet.

Making matters worse for passive bondholders is that borrowing costs for governments and companies included in benchmarks fall as index-tracking funds attract more assets. This, in turn, incentivises even more borrowing – a development the BIS describes as a systemic risk.

Having a clear idea of credit risk is especially problematic for investors in corporate bond indices. As new bonds are absorbed into the benchmark, the creditworthiness of the index can sometimes change dramatically. A credit rating downgrade of a large company can have a significant bearing on the credit profile of the entire benchmark.

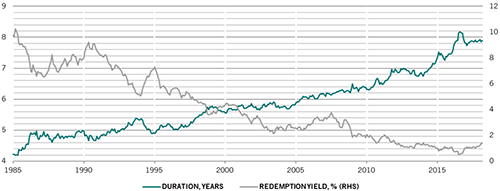

A POOR TRADE-OFF: BOND INDICES' YIELDS ARE LOW WHILE THEIR VULNERABILITY TO RATE RISES IS HIGH

Duration and yield of Citgroup's G7 world government bond index

(Source: Pictet Asset Management, Datastream. Data covering period 31.01.1995 – 30.03.2018.)

But being helpless in the face of a sudden shift in a bond issuer’s creditworthiness is not the only landmine passive investors face. Higher interest rates are another.

The duration of the Barclays Global Aggregate Index for instance – one of the most widely used bond indices – has climbed to 7.0 years, from 5.4 years a decade ago.

This amounts to a near-doubling of the interest rate risk that is embedded in bond indices. That this is the case at a time when interest rates in the US and some other parts of the world have started to rise is worrying.

Higher trading costs also make bond indexation difficult. The turnover bond indices typically experience from one year to the next is considerable, far higher than that of equity benchmarks, and ranging between 30 and 70 per cent. For high- yield bond indices, it can be as much as 90 per cent. Tracking a bond index therefore requires a lot of trading, which increases investment costs. These costs have been estimated to be around 0.3 per cent per year for an aggregate bond index. Costs for lower-rated corporate or emerging market debt can be substantially higher. These implementation costs are rarely debated, yet are major flaw in index-tracking bond funds.

Finally, because regional or global bond indices can include up to 5,000 separate securities, indexation relies more often than not on sampling. But building an index in this way often involves using substitutes. In other words, to offset various costs, index managers often substitute bonds of higher quality but lower yield with ones of higher risk and lower quality. It is for this reason that index-tracker funds often experience sharper falls than their reference indices during bouts of market turbulence.

There is, then, nothing dull about passive bond funds. And that’s not a good thing.

Diesen Beitrag teilen: