Janus Henderson: Will Chinese policy easing work?

Satisfactory Chinese activity numbers for the first quarter / March are consistent with monetary trends in mid-2017. Subsequent monetary weakness, which continued in March, suggests a significant slowdown over the remainder of 2018.

26.04.2018 | 12:10 Uhr

The authorities appear to be shifting tack to head off economic weakness. Late cycle policy easing can prove counter-productive by boosting prices, thereby exerting additional downward pressure on real money trends.

The authorities appear to be shifting tack to head off economic weakness. Late cycle policy easing can prove counter-productive by boosting prices, thereby exerting additional downward pressure on real money trends.

This week’s activity numbers were mostly solid, although annual industrial output growth fell to a seven-month low as an upward distortion from the late timing of the Chinese New Year unwound (discussed in a previous post).

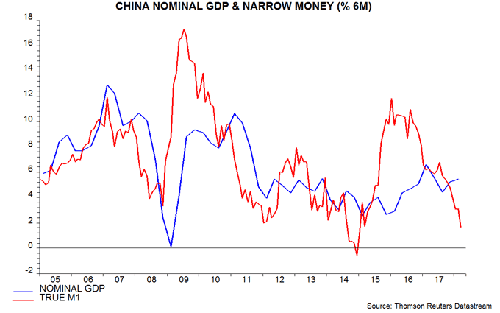

Two-quarter growth of nominal GDP, seasonally adjusted, rose slightly further last quarter, consistent with a stabilisation / small recovery in six-month narrow money expansion in mid-2017 – see first chart.

Narrow money trends, however, weakened sharply after September, with six-month growth falling further in March to its lowest since January 2015, suggesting a significant loss of economic momentum alongside weaker inflationary pressures through late 2018.

Credit trends are also concerning: the percentage increase in the stock of “total social financing” in the first quarter, of 3.2%, was the lowest on record in data extending back to 2004.

The authorities, therefore, appear to be moving to ease policy. A fall in term interbank rates in early April suggested that a shift was under way and this week’s reduction in the reserve requirement ratio for a range of banks, involving a net increase in liquidity supply, offers confirmation.

Market perceptions of a Chinese policy turnaround may have driven this month’s recovery in risk assets and contributed to renewed strength in commodity prices.

As previously discussed, Chinese loosening, together with a recovery in US narrow money growth in lagged response to tax cuts, could result in a revival in the global real money growth measure tracked here. Late cycle policy easing, however, can be ineffective or even counter-productive, feeding directly into higher prices without boosting nominal money trends.

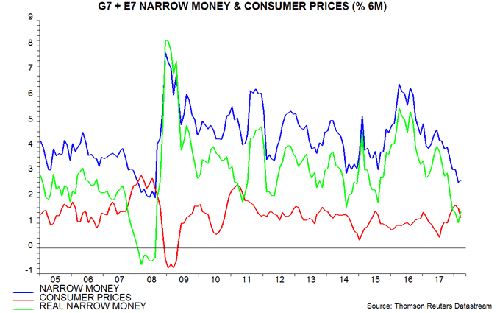

The US FOMC was not, as is sometimes claimed, asleep at the wheel in the run-up to the 2008-09 recession – it cut the fed funds target rate by 100 basis points between August and December 2007, with the US recession beginning in January 2008, according to the NBER. Policy easing, however, contributed to a surge in commodity prices that continued into mid-2008. This surge fed through into global consumer prices and, with nominal money trends remaining weak, was an important reason for the six-month change in real narrow money turning negative – second chart.

Diesen Beitrag teilen: