Janus Henderson: Is China starting to ease?

Previous posts (e.g. here) suggested that weaker economic growth and a cooling of inflationary pressures would prompt the Chinese authorities to take steps to ease monetary conditions in mid-2018. A recent fall in interbank rates could be an early indication that a policy shift is under way.

09.04.2018 | 10:46 Uhr

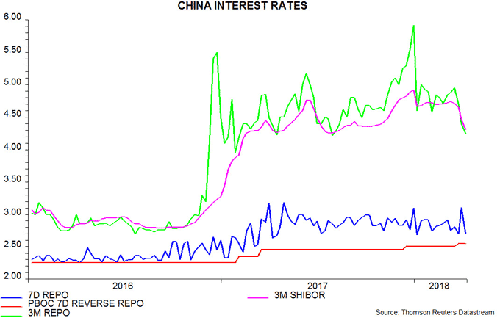

Significant policy tightening since late 2016 has been achieved mainly via regulatory / macroprudential measures, rather that Western-style changes in central bank money market intervention rates. The PBoC seven-day reverse repo rate, which sets the floor for short-term market rates, rose by only 25 basis points (bp) between end-September 2016 and end-December 2017. The regulatory clampdown, however, restricted access to and boosted the cost of term market funding. Three-month SHIBOR climbed 210 bp over the same period. Restrictive policy, that is, has operated to a significant extent through the wider three-month SHIBOR / seven-day reverse repo rate spread.

Significant policy tightening since late 2016 has been achieved mainly via regulatory / macroprudential measures, rather that Western-style changes in central bank money market intervention rates. The PBoC seven-day reverse repo rate, which sets the floor for short-term market rates, rose by only 25 basis points (bp) between end-September 2016 and end-December 2017. The regulatory clampdown, however, restricted access to and boosted the cost of term market funding. Three-month SHIBOR climbed 210 bp over the same period. Restrictive policy, that is, has operated to a significant extent through the wider three-month SHIBOR / seven-day reverse repo rate spread.

A recent fall in the spread, therefore, may be meaningful. The PBoC raised the seven-day reverse repo rate by a further 5 bp on 22 March following the latest FOMC quarter-point hike, contributing to a consensus view that policy remains on a tightening tack. Three-month SHIBOR, however, has, fallen by 30 bp since 21 March, reducing the spread to the lowest since July – see first chart.

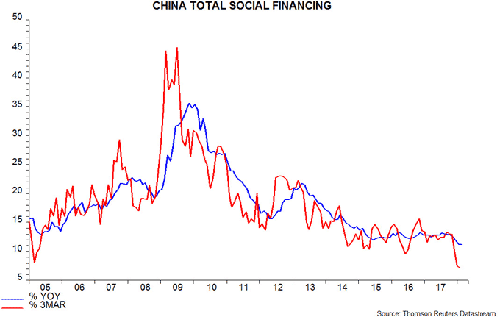

Recent economic news, admittedly, has been mixed and not obviously a trigger for a policy shift towards easing. The authorities, however, may be concerned about a continued slowdown in credit and monetary aggregates: three-month annualised growth of total social financing, seasonally adjusted by Datastream, fell to a new low of 7.1% in February – second chart. Producer price pressures, meanwhile, have cooled, with input price balances in the March NBS and Markit manufacturing PMI surveys at nine-month lows. Rising trade tensions with the US may also be shifting policy-makers’ bias towards precautionary easing.

Policy easing, if confirmed, would be expected, as usual, to be reflected swiftly in a revival in money trends, in turn suggesting improving economic prospects for late 2018 / early 2019. If accompanied by a stabilisation or recovery in US money trends, which – as previously discussed – would be consistent with experience after previous large tax cuts, this would temper concern here that an expected global economic slowdown over the remainder of 2018 will extend and deepen in 2019.

Diesen Beitrag teilen: