BNP Paribas AM: Don’t buy the index

The index yield (JPMorgan Government Bond Index Emerging Markets) is at its lowest since the ‘taper tantrum’. There have been flows into EM fixed income and, according to JPMorgan, cumulative inflows into the asset class totaled USD.

24.10.2017 | 12:56 Uhr

Despite heightened geopolitical uncertainty and a 50 basis points increase in the US fed funds rate this year, emerging market local currency bond yields have declined by 80 basis points and outperformed the benchmark 10-year US Treasury bond by 60 basis points. In fact, the index yield (JPMorgan Government Bond Index- Emerging Markets (GBI-EM)) is currently at its lowest since the ‘taper tantrum’. How did we get here and will it continue? Several factors have contributed to this year’s outperformance:

1. Favorable index composition

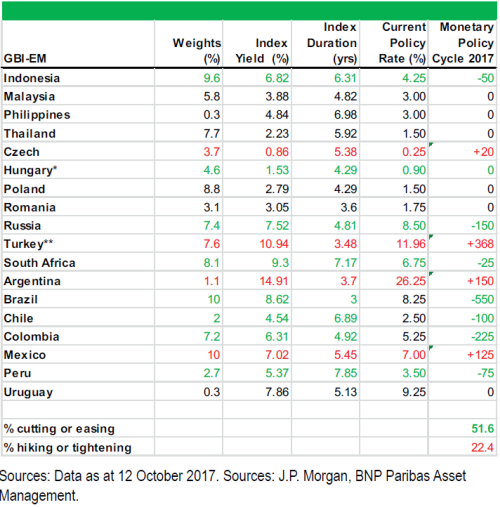

The key theme in EM local currency bonds this year has been dispersion. This is a story of two different EMs currently unfolding: declining inflation in high-yielding countries coexists with rising or bottoming inflation in low-yielding countries. Declining inflation has allowed central banks to cut interest rates from very high levels. These countries account for just over 50% of the GBI-EM Index, while countries where policy rates have risen account for 22%. So in the index, the high-yielding rate cutters dominate. In addition, policy rate increases in Mexico, Argentina and Turkey (with a combined 18.7% weight) were perceived in the financial markets as having increased central bank credibility, resulting in a rally in the medium to longer-term segments of the local yield curves for most of the year. Regionally, the decline in yields has been driven by Latin America and emerging Europe (see Figure 1).

Figure 1. GBI-EM constituent statistics

2. Supportive global factors

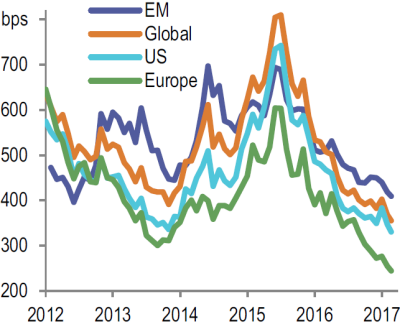

The global macroeconomic environment has been supportive of EM bonds. Global growth has been revised up during the year (although the most recent revisions were downward) and leading indicators point to continued strong momentum. Meanwhile, inflation has been surprising on the downside. In addition, trade volumes and prices have risen this year, which, historically, have a multiplier effect on EM growth and a positive impact on their currencies through the terms of trade. Furthermore, rich valuations in other asset classes have attracted flows into EM fixed income. According to JPMorgan, cumulative inflows into the asset class totaled USD 77.1 billion by September and were forecast to exceed USD 110 billion by the end of the year. That level would surpass the record of USD 103 billion in 2012. Flows have been driven by both traditional EM debt investors as well as crossover investors (see Figure 2).

Figure 2. Global high yield index spreads

Outlook for 2018

Unlike 2017, we foresee a less clear-cut macroeconomic theme for 2018. Alpha generation and country-level dispersion will likely prove much stronger themes. Most of the EM countries cutting interest rates are at the tail end of their monetary cycles, but further policy easing is still expected in Russia, Brazil and, potentially, Colombia. South Africa has only just begun cutting rates. Mexico and Turkey are the only countries which will likely have sharply declining inflation next year, but the extent of monetary easing there can be expected to depend on geopolitics and inflation. In addition, some countries could be raising policy rates next year, such as the Czech Republic and Romania, but these are small index components and monetary policy tightening there is already expected.

In our view, the bottom-line is that the strong tailwinds that drove EM yields markedly lower this year are likely to be less pronounced in the near term, although on the whole, yields can continue to grind lower. We expect EM yields to become more sensitive to idiosyncratic factors. Investors are also more likely to maximize interest income if capital appreciation opportunities are no longer as obvious.

Global factors

The growth environment should remain supportive, with Latin America forecast to see the largest year-on-year increase in GDP growth in 2018. The EM inflation outlook is also benign with inflation remaining within the target range for most countries at the end of next year. This may look like a continuation of the environment we saw in 2017, but there are two key differences that investors should take into account in 2018.

The first concerns the efforts by the G4 central bank to shrink their balance sheets, which can be expected to take effect towards the middle of the year. Historical data suggests that much of the flows in and out of EM bonds can be explained by global liquidity conditions in general and central bank balance sheet changes in particular. The second is global inflation, and particularly US inflation. This has been a key pillar of the benign environment despite the various interest-rate rises by the US Federal Reserve. Any sign that a strong US labor market and increased wage growth are spilling over into higher underlying inflation would lead to a reassessment of the framework that markets have become accustomed to over the past several years.

Diesen Beitrag teilen: