Schroders: Why interest rates predictions have suddenly shifted

The market forecast for the first rise in UK interest rates has moved closer. We explain why.

11.07.2017 | 08:10 Uhr

Pressure is building for interest rates to be raised in the UK following a surge in inflation to a five-year high.

Why are there fresh calls for rate rise?

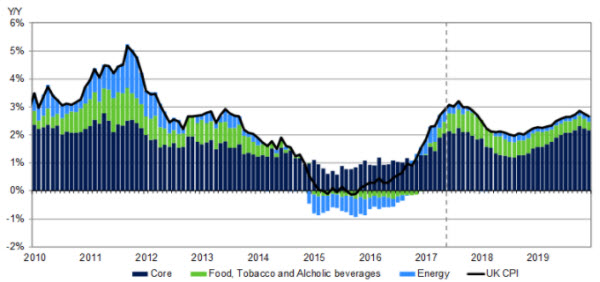

The Bank of England’s monetary policy committee (MPC) is tasked with keeping inflation at around 2% in the years ahead. But the consumer prices index (CPI) climbed to 2.9% in May, up from 1.8% at the start of the year.

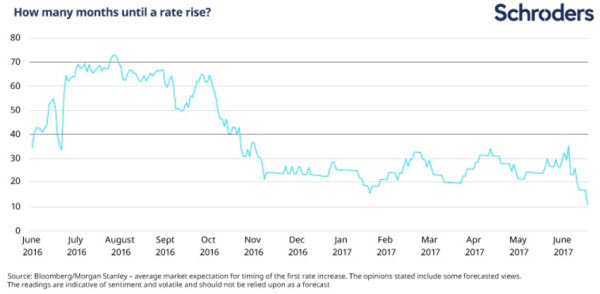

The surge in inflation has caught markets by surprise and led to a shift in expectations for rates. Markets, as of 6 July, expected the Bank of England to order the first increase as soon as January 2018.

Only a month earlier, the expectation had been for a delay in raising rates until the summer of 2019.

At the June meeting of the MPC, three of the members voted for a quarter-point rise while five, including Governor Mark Carney, opted for holding the bank rate at 0.25%.

*Source: Bloomberg. Based on overnight index swaps, implied pricing as of 10/07/2017. The readings are indicative of sentiment and volatile and should not be relied upon as a forecast.

Will more MPC members vote for a rise?

One of those to vote for a rise, Kristin Forbes, has now stepped down. She will be replaced on the committee by Silvana Tenreyro, a professor at the London School of Economics. Her voting intentions are unknown.

Andy Haldane, chief economist at the Bank and an MPC member, voted to hold but has since made comments that could signal a change of heart. He said: "Provided the data are still on track, I do think that beginning the process of withdrawing some of the incremental stimulus provided last August would be prudent moving into the second half of the year.”

Carney’s comments late last month were also seen by markets as a shift in opinion. He said: “Some removal of monetary stimulus is likely to become necessary if the trade-off facing the MPC continues to lessen and the policy decision accordingly becomes more conventional.”

The pound rose from $1.28 to nearly $1.30 when markets digested the governor’s speech (the prospect of higher rates makes the pound more attractive to foreign investors and tends to push it higher).

Why might rates stay on hold?

The MPC faces a dilemma. Inflation is above its target and rising but at the same time, the economy is slowing. The impact of Brexit on the economy is something else for the committee to consider. Inflation has risen as a result of the EU referendum result weakening the pound.

Further out, the Brexit negotiations may weaken confidence and the economy could falter. The fragile state of the UK government, following the general election, might be another consideration.

Some MPC members may regard these risks as being too great and keep voting “hold”.

Ultimately, the question is what will happen to inflation. The Schroders Economics Group forecasts inflation will exceed 3% over the summer before falling back below the 2% target in early 2018.

Schroders UK CPI inflation forecast

Source: Schroders Economics Group. 30 June 2017.The opinions stated include some forecasted views. We believe that we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee that any forecasts or opinions will be realised.

Azad Zangana, Senior European Economist and Strategist, said: “The sharp rise in inflation has coincided with a slowdown in economic growth along with wage growth.

“While jobs are still being created for now, higher inflation has reduced the disposable income of households, and therefore has contributed to the slowdown in spending.

“The Bank of England has to decide whether the inflation the UK is experiencing at present is temporary or permanent.

"For most on the committee, the rise in inflation caused by the depreciation in sterling should be a temporary phenomenon. However, the more hawkish minority of members see a risk that wages could accelerate in response, causing even more inflation in the future.”

When was the last adjustment to interest rates?

In response to the Brexit verdict of last June’s EU referendum, the MPC cut the UK bank rate from 0.50% - its level for more than eight years - to 0.25% in August.

The market expectation after last summer's cut was that rates wouldn’t rise again until 2021, although trading is highly volatile over longer timeframes and shouldn’t be relied upon as guidance.

The chart below captures how long the market expects to wait for a rate rise at various points over the past 18 months.

How would a rate rise affect me?

Mortgages

The bank rate affects wider borrowing costs, but not always directly. Some mortgage deals are linked to the rate and would rise immediately but the standard variable rates, or SVRs, that most borrowers pay are set at discretion of the lender.

The pricing of new fixed mortgage deals is influenced by market expectation. The wholesale cost of five-year fixed-rate money, known as “swaps”, has risen sharply in the past month, up from 0.77% in early June to more than 1% in early July.

Savings

Savings rates are also influenced by the bank rate and should improve if the MPC acts. It would be welcome relief given the average instant access savings account only pays 0.15%, including bonuses, according to Bank of England data. The average account paid 0.45% a year earlier.

For investors, bond prices traditionally suffer when rates rise, or even just on the anticipation of an increase. This is because the fixed payments made by companies - or the UK government - on their bonds is less attractive when investors are being offered improving rates of interest elsewhere. However, it is impossible to forecast future market returns.

Dieser Artikel wurde am 10.07.17 auf schroders.com veröffentlicht.

Diesen Beitrag teilen: