Henderson: Is the Fed misreading the economy (again)?

The path to higher rates is unlikely to be smooth and the risks to the Fed’s guidance for the level of rates at end-2017 are judged here to be weighted modestly to the downside, based on current monetary trends.

19.12.2016 | 15:15 Uhr

The Federal Reserve delivered the expected quarter-point rise to 0.625% in the federal funds rate* and signalled a modest hawkish shift in its policy intentions, with the median assessment of the 17 meeting participants of the appropriate funds rate at end-2017 rising from 1.125% in September to 1.375%. The median forecast overstates the collective change of view – the mean assessment rose by only 6 basis points (bp), i.e. from 1.31% to 1.37%. The shift reflects recent mostly-solid economic data – in particular, a further fall in the unemployment rate to 4.6% – and an increased probablility of fiscal stimulus. A cynic might suggest, in addition, that some Committee members previously suppressed more hawkish intentions in an effort to support the status quo candidate in the presidential election.

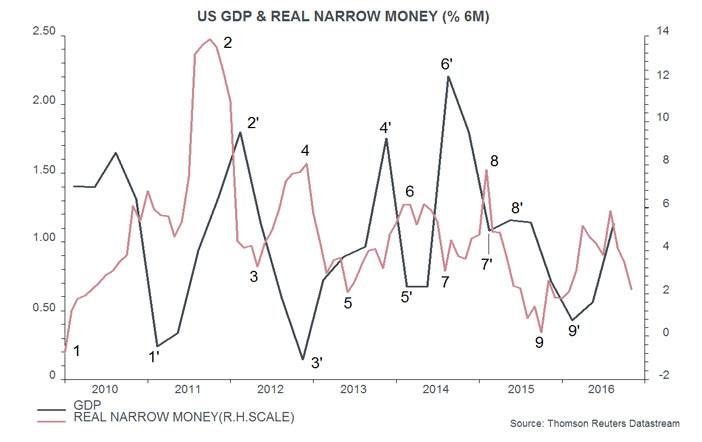

The Fed’s policy guidance often proves unreliable, particularly when it conflicts with monetary trends. The median forecast in December 2015 was for a 100 bp rise in rates during 2016, despite real narrow money slowing sharply into late 2015, signalling that economic growth was likely to disappoint. It did, and the Fed was forced to backtrack.

Narrow money rebounded strongly in early 2016 but is now slowing again, though less dramatically than in 2015. Six-month growth of real narrow money peaked in August 2016 and fell further in November, to its lowest since February. Allowing for an average nine-month lead, the suggestion is that the economy will remain solid through spring 2017, possibly supporting two quarter-point Fed hikes during the first half, but will lose momentum in the summer.

A hawkish counterargument is that fiscal stimulus will sustain robust economic growth later in 2017 and in 2018. The view here, however, is that the effects of fiscal policy are incorporated in narrow money trends: shifts in money demand are largely driven by changes in spending intentions of households and firms, which would strengthen in response to an effective fiscal stimulus. Narrow money growth, in other words, would need to rise in early 2017 to support the hawkish view. Even if it does, the recent slowdown suggests a “soft patch” for the economy next summer.

*Mid-point of target range.

Die Wertentwicklung in der Vergangenheit ist kein zuverlässiger Indikator für die künftige Wertentwicklung. Alle Performance-Angaben beinhalten Erträge und Kapitalgewinne bzw. -verluste, aber keine wiederkehrenden Gebühren oder sonstigen Ausgaben des Fond.

Die Informationen in diesem Artikel stellen keine Anlageberatung dar.

Diesen Beitrag teilen: