Janus Henderson: Euroland "basic balance" deterioration suggesting weaker euro

Euro appreciation in 2017 was underpinned by a strengthening of the Euroland basic balance of payments position. The basic balance has deteriorated recently and credit / money trends suggest further weakness. Downside risk for the currency, therefore, has increased.

22.05.2018 | 12:46 Uhr

The “monetarist” approach to assessing currency prospects assumes that:

The “monetarist” approach to assessing currency prospects assumes that:

1) major currency swings are caused by changes in the basic balance, defined as the sum of the current account and net direct and portfolio capital flows; and

2) movements in the basic balance are caused by changes in the differential between the expansion of domestic bank credit and the growth rate of money and other domestic bank liabilities.

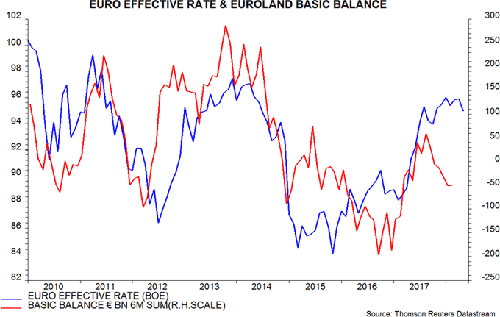

On 1), the first chart below shows the Bank of England’s euro effective exchange rate together with the Euroland basic balance, calculated on a six-month rolling basis. A positive relationship is apparent, with the basic balance sometimes leading currency swings. Euro strength in 2017 was associated with a turnaround in the basic balance from a large deficit into surplus. This improvement partially reversed in late 2017 / early 2018. The euro’s recent decline may reflect this reversal.

On 2), the basic balance mirrors – by accounting definition – changes in the net external assets of the banking system (including the monetary authority). This is because a basic balance surplus or deficit necessitates an offsetting flow of funds through the banks.

The change in banks’ net external assets, meanwhile, is equal to – again by accounting definition – the difference between their new domestic funding (i.e. money and other liabilities, including capital and reserves) and domestic credit expansion. A surplus of domestic funding relative to lending, for example, is reflected in a flow of funds overseas and a rise in net external assets.

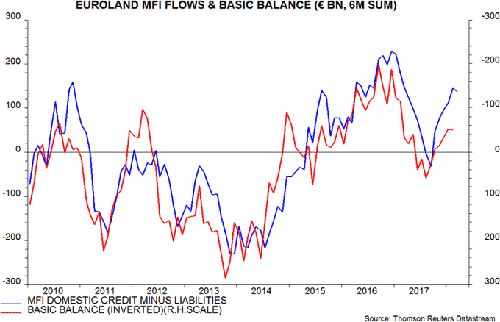

The second chart shows the gap between domestic credit and funding flows of “monetary financial institutions” (MFIs) and the basic balance, plotted inverted. The relationship is not exact because the definitions of the series do not exactly correspond to theory and because of measurement error.

The monetarist approach assumes that this relationship is causal, i.e. changes in the balance between domestic credit and funding flows determine changes in the basic balance, which in turn drive currency movements.

The monetarist approach was the basis for a suggestion here in January 2017 that the euro (as well as the yen and renminbi) would rise against the US dollar in 2017. The thinking was that the ECB’s wind-down of QE would curb domestic credit expansion, while stronger economic growth would boost the demand to hold money and other bank liabilities. A narrowing of the gap between domestic credit expansion and domestic funding growth would strengthen the basic balance and boost the euro.

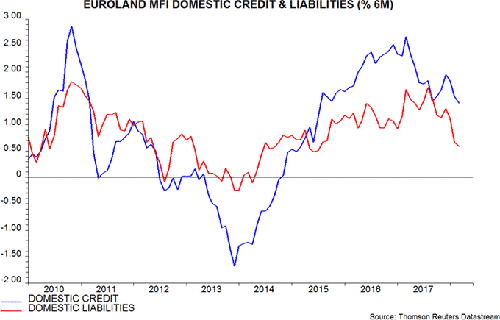

This scenario played out, with six-month rates of increase of domestic credit and domestic liabilities converging in August / September 2017 – third chart.

A follow-up post in December, however, suggested that the balance between domestic credit and funding flows would turn negative for the euro in 2018, reflecting the ECB’s tardiness in normalising monetary policy. The slow pace of QE wind-down coupled with a likely firming of private lending growth would limit a further decline in domestic credit expansion, while the refusal to adjust policy rates to reflect a stronger economy and 1-2% inflation was likely to depress demand for bank liabilities.

Recent trends are consistent with this forecast, with growth of domestic liabilities falling with credit expansion little changed, and the basic balance moving back into deficit. The assessment of the December post still appears valid, with a possibility that the ECB will delay ending QE and push back a rate rise even further in response to recent softer activity data, a fall in core consumer price inflation and renewed concern about Italian political and economic instability.

The monetarist approach, by contrast, suggests a positive outlook for the US dollar, with the Fed’s QE reversal plans implying an increasing drag on domestic credit expansion and money demand likely to be boosted by rising interest rates.

Diesen Beitrag teilen: