NN IP: Mario Draghi maintains a steady but flexible hand

The “mini taper tantrum” that followed Mario Draghi’s words in late June proved that central bankers have to walk a tightrope in order to not causing markets to shift their policy expectations too much. Draghi therefore kept his cards close to his chest after the latest ECB meeting.

28.07.2017 | 09:30 Uhr

The tightrope central bankers have to walk

Central banks have acted as big market movers over the past few weeks. Before we delve into the policy meetings of the ECB and Bank of Japan we will repeat our main conclusions from the mini taper tantrum which occurred after Draghi’s Sintra speech.

Central bankers walk a tightrope between two issues. On the one hand they want to express their confidence in the robustness of the recovery because this will shore up confidence and support easy financial conditions. On the other hand they want to signal that their response to the growth outlook will be very muted and gradual, to prevent markets from getting carried away in pricing in tighter monetary policy. An important driver here is the strong persistence of downside inflation surprises.

At the same time, central bankers face costs attached to unconventional policy in terms of a drag on the profitability/ return of financials and pension funds, political costs (opposition to low interest rates) and QE scarcity constraints. The improved growth outlook changes the QE cost/benefit trade-off and, as a result, central bankers feel they should cautiously and gradually change the future trajectory of the size of their balance sheet. This holds all the more so because an improving economy endogenously makes policy more expansionary by raising r-star (the real policy rate consistent with full employment) and hopefully also inflation expectations.

In this process of gradually adjusting the policy stance, central bankers run into the problem that private sector expectations of future policy have no anchor in the form of past experience to which the market can benchmark central bank action in unconventional space. Because of this, even a hint of a small policy change can cause an unwarranted big hawkish shift in the expected future monetary policy stance. This may even force the central bank to backtrack and stay lower for longer than initially intended. As central bankers learn to deal with this problem their emphasis on prudence and gradualism increases.

As growth momentum becomes more robust central bankers seem to become somewhat more tolerant in allowing an inflation undershoot. This is both because most of them have a dual mandate (better growth performance thus compensates for worse inflation performance) and because they believe the Phillips curve will kick in at some point (i.e. better growth will push inflation higher with a lag). The risk of this strategy is clearly that inflation expectations will drift down further if the Phillips curve mechanism is weaker than in the past for structural reasons (e.g. the combination of globalisation and rapid technological change in some sectors).

The aforementioned costs attached to QE have weakened the link between QE policy action and price stability, but they probably have not completely broken it. Central banks will probably try to compensate for this weaker link by enhancing their forward guidance on rates. Hence, the longer inflation remains subdued the more rates will be lower for even longer.

Draghi maintains a steady but flexible hand

With these points in mind we can analyse the ECB press conference. The most important point to take away is that Draghi pretty much tried to avoid putting more fuel on the hawkish flames that dominated market thinking in the aftermath of his Sintra speech in June. We see this as confirmation that the market indeed got a bit carried away because Draghi essentially said nothing new in Sintra.

First of all, there was no change whatsoever to the policy parameters. The minutes of the June meeting revealed that there had been some discussion about removing the easing bias on QE but the ECB decided to retain it in July. In fact, keeping the QE easing bias carries little cost for the ECB because it describes what the ECB would do if downside risks were to materialize. In addition to this, the ECB retained the guidance that rates will remain at present levels until “well past” the completion of asset purchases. There has been a lot of speculation about this aspect of rate forward guidance and many pundits expect the “well past” bit to be removed at some point, because that will enable the ECB to hike the negative depo rate soon after the end of QE.

In this respect, one should bear in mind that the negative depo rate acts as a tax on the core banking system because this is where the excess reserves created by QE have been accumulated. The depo rate will act as the most important benchmark policy rate as long as there is a large amount of excess reserves in the system. For this reason we do not believe the ECB could get away with a strategy of retaining the “well past” language, saying it only applies to the refi rate (currently 0%) and hiking the depo rate (currently -0.4%) soon after the end of QE.

A difficult choice will have to be made here because tapering implies that more of the burden of keeping financial conditions at easy levels will be put on rate forward guidance. If inflation continues to surprise on the downside this rate guidance will have to move in the direction of “lower for even longer”. A further dovish element was that Draghi stated that there has been no sustainable and self-sustained upward adjustment in underlying inflation yet because of which “the three Ps” – prudence, patience and persistence – continue to apply. This refers respectively to proceeding cautiously and gradually when it comes to adjusting the policy parameters, a recognition that it will take time before the Phillips curve kicks in and that, therefore, the ECB will stick to the current policy course for some time to come.

In addition to all this, it is also clear that the ECB places great value on retaining a fair degree of flexibility in the question as to how and when to adjust its policy parameters. This makes a lot of sense given the uncertainty about when and to what extent inflation will pick up as well as other known and unknown unknowns which could trigger substantial movements in financial conditions (e.g. actions by other central banks and political risks). Hence, Draghi kept the timing of the tapering announcement deliberately vague by saying this would happen “in the autumn”. This could either mean September or October and we have some sympathy for the latter for two reasons.

First of all, it will afford more time to assess the momentum of underlying inflation. If progress is not satisfactory, the doves will have a stronger hand in pushing for a more gradual taper which would surely be of the “slow and stretch” kind (i.e. lowering the pace a bit for 3 or 6 months and no announcement yet of an end date). In this respect, Draghi made it clear that size and duration of QE will remain linked to progress towards the inflation target (even though we believe this link is weaker than it was in the past). Secondly, the October meeting will of course take place after the Fed September meeting, which is important because the Fed is likely to start balance sheet roll-off at that meeting. This will give the ECB a valuable opportunity to take the effects of Fed action on global term premiums into account.

Not surprisingly, the ECB also remains completely silent on how tapering will proceed. Draghi did not even say that the relevant committees have been instructed to assess the various options. We believe the ECB will also seek to maintain a large degree of flexibility here which may even result in QE extending into 2019. Such as scenario could happen if inflation continues to disappoint on the downside (which would not surprise us). In that case the ECB may wish to increase the credibility of the “lower for even longer” rate guidance by backing up its words with action in the form of ongoing purchases (albeit at a very low pace to avoid scarcity constraints). This action could well be effective in making rate guidance more credible, especially if the ECB retains the “well past” language in its rate forward guidance.

Bank of Japan lowers inflation forecast

The BoJ takes a somewhat different approach than the Fed and the ECB. In a sense it retains a strong link between the continuation of QE and the achievement of the inflation target. Actually this link is very strong because QE will continue until the BoJ has achieved a persistent but moderate overshoot of the target. Given where Japanese inflation expectations are now, this suggests ongoing QE well into the next decade. Nevertheless, at the same time the link between QE and the inflation target has become a lot more volatile because the BoJ has inserted an intermediate target in between in the form of Yield Curve Control. This makes the volume of QE pretty much endogenous to the supply and demand balance in the 0-10y bucket of the JGB yield curve.

The main message of the July BoJ meeting was that the central bank downgraded its inflation forecasts and now expects to hit the target at a later date. The main reason behind this is probably recognition that below-target inflation expectations are stickier than the BoJ believed at first. The BoJ’s inflation forecast is now thus more realistic. At the same time this move suggests that yield curve control and the associated balance sheet expansion will be around for longer, which can be seen as a form of pushback against pundits in Japan who have been arguing that the BoJ should explain its exit strategy sooner rather than later. Kuroda flatly refused to talk about the exit, which is pretty wise given the experience of the taper tantrum and Draghi’s Sintra speech. We do not expect the BoJ to change the 10y yield target until several indicators of actual and expected inflation pass the 1% threshold, which will probably not be until sometime in 2018. Kuroda’s dovish influence in the BoJ Board was enhanced by the appointment of two new members with a dovish view on policy. Obviously this increases our confidence in our BoJ call.

Emerging markets: improving growth prospects

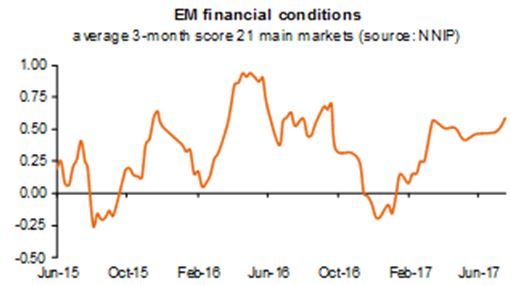

The EM growth recovery continues. The global trade pick-up remains a key driver, which is partly the result of continuously good growth dynamics in China. And meanwhile, the recovery in capital flows to EM is the main reason why financial conditions in EM continue to ease. This is producing the first meaningful pick-up in EM credit growth since the 2009-2011 post-Lehman boom (in EM ex-China that is). Stronger credit growth (from 6% in Q1’17 to 8% now) should help to give the domestic demand recovery legs in the coming quarters.

Our own financial conditions indicator, which captures the change in policy rates, market interest rates, money supply, fiscal policy, fiscal policy expectations, effective exchange rates and capital flows for the 21 main emerging economies, remains in positive territory and even improved again in the past weeks (see graph). Meanwhile, our economic growth momentum indicator continues its positive trend it has been in for more than a year now.

Diesen Beitrag teilen: