Janus Henderson: US ISM strength: signal or "head fake"?

Last week the US ISM manufacturing purchasing managers' index rose to a new 34-month high. What are the implications for the markets?

17.07.2017 | 12:48 Uhr

A rise in the US ISM manufacturing purchasing managers’ index to a 34-month high in June, reported last week, presents a challenge to the view here that global economic momentum peaked in spring 2017 and will moderate into the fourth quarter. The ISM PMI is widely regarded as a reliable gauge of global as well US industrial activity; indeed, it exhibits a slightly higher correlation with global than US industrial output growth*.

A provisional judgement is that the ISM surge is a reflection of earlier economic strength and will be swiftly reversed. This is supported by three observations.

First, the forward-looking new orders component of the PMI, while rising sharply in June, remained below its level in February / March.

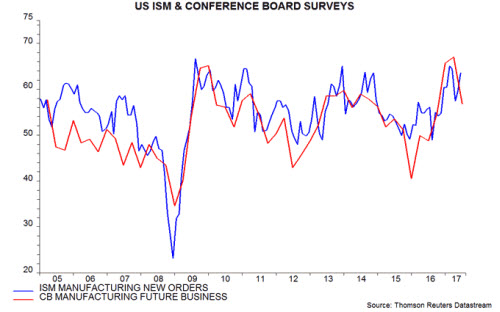

Secondly, the ISM surge is at odds with the Conference Board CEO confidence survey for the second quarter, also released last week, which reported weaker business expectations among manufacturers. The CEO expectations measure usually aligns with the trend in ISM new orders – see first chart.

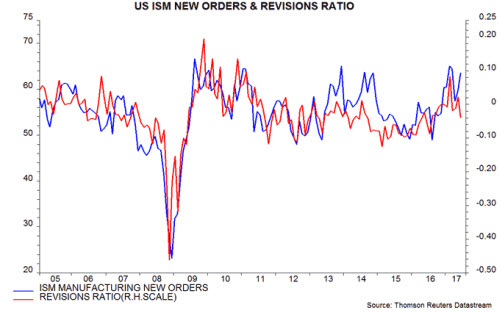

Thirdly, the ISM result also contrasts with a fall in the IBES US equity analysts’ earnings revisions ratio in June, to an 11-month low. A rise in the revisions ratio in May had suggested that ISM new orders would rebound in June – second chart.

As previously discussed, the global slowdown is expected to be modest and temporary, with money trends now signalling economic reacceleration in late 2017. Near-term negative economic surprises may focus on Euroland, partly reflecting consensus over-optimism.

*Contemporaneous correlation with six-month industrial output growth over 1996-2016: global (i.e. G7 plus E7) +0.77, US +0.71.

Diesen Beitrag teilen: