Janus Henderson: Forecasting rule suggesting stable UK growth

A simple forecasting rule-of-thumb based on money growth and share prices is giving a neutral message for 2018 economic prospects.

15.12.2017 | 12:40 Uhr

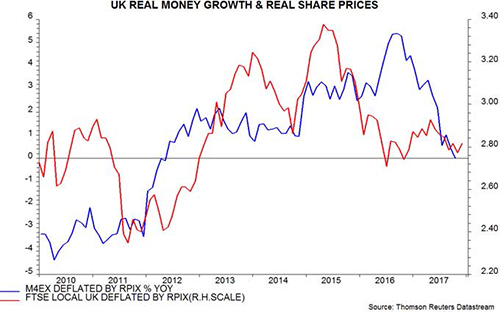

The forecasting rule classifies the outlook for GDP growth in the following calendar year as good, bad or average depending on whether December levels of real (i.e. inflation-adjusted) money growth and share prices are higher or lower than 12 months earlier. Real money growth is measured by the annual rate of change of the broad M4ex measure deflated by the retail prices index excluding mortgage interest (RPIX). Share prices are measured by the FTSE local UK index, constituents of which derive at least 70% of sales from the UK and the rest of Europe, again deflated by the December RPIX*.

The forecasting rule classifies the outlook for GDP growth in the following calendar year as good, bad or average depending on whether December levels of real (i.e. inflation-adjusted) money growth and share prices are higher or lower than 12 months earlier. Real money growth is measured by the annual rate of change of the broad M4ex measure deflated by the retail prices index excluding mortgage interest (RPIX). Share prices are measured by the FTSE local UK index, constituents of which derive at least 70% of sales from the UK and the rest of Europe, again deflated by the December RPIX*.

Annual GDP growth averaged 2.3% in the 51 calendar years from 1966 to 2016. The forecasting rule gave a “double-positive” signal for 16 of these years (i.e. both real money growth and share prices at the end of the prior year were higher than 12 months before). GDP growth in these years averaged 3.8%.

There were, by contrast, 11 years for which the forecasting rule gave a “double-negative” signal. Growth in these years averaged just 0.3%. In the remaining 24 years for which the money supply and share prices gave conflicting signals, GDP expansion averaged 2.3%, in line with the long-term mean.

The rule has continued to perform respectably in recent years. A double-negative warning was given at end-2008 ahead of a 4.2% GDP slump in 2009. A double-positive at end-2012, meanwhile, signalled that growth would pick up significantly in 2013 – contrary to prevailing angst about a double-dip recession.

The rule suggested that 2017 would be an average year: real M4ex growth rose from 2.5% to 4.5% between December 2015 and December 2016 but real share prices fell by 10.4% – the FTSE local UK index, unlike the FTSE 100 and all-share indices, did not enjoy a currency-driven “Brexit bounce”**. The average GDP growth outcome historically for this combination was 1.9%. The current consensus estimate of 2017 GDP growth is 1.6% – below the average but above a consensus forecast of 1.2% in December 2016***.

The rule is also giving a neutral message for 2018, although this will not be confirmed until late January, when December monetary data are released. As of October, annual real M4ex growth had fallen to zero, from 4.5% in December 2016 – see chart. The average level of the FTSE local UK index so far in December, meanwhile, is 4.3% higher than in December 2016. Assuming that annual RPIX inflation in December is equal to or lower than its November level of 4.0%, therefore, real share prices are on course for a marginal annual gain.

The average GDP growth outcome historically for the combination of negative monetary and positive share price signals was 2.4%. The current consensus forecast for 2018 is significantly weaker, at 1.4%.

A double-negative combination is still possible, though unlikely. The FTSE local UK index would need to average 2% less than yesterday’s level (13 December) over the remainder of the month to result in a real-terms decline compared with December 2016, assuming stable RPIX inflation.

* The FTSE local UK index goes back to 1994. The FT 30 index, which is also domestically orientated, was used for earlier years.

** Local UK stocks account for only 22% of the market capitalisation of the FTSE all-share index.

*** Consensus numbers from the Treasury’s monthly survey of forecasters.

Diesen Beitrag teilen: