Janus Henderson: Euroland economic news softening on schedule

Money trends, by contrast, suggest a further significant cooling over coming months, so Simon Ward, SimonWard, Chief Economist at Janus Henderson.

26.02.2018 | 12:45 Uhr

Previous posts (e.g. here) argued that the Euroland economy would slow from around spring 2018. Weaker February PMI results are consistent with this forecast. As usual at economic momentum peaks, the consensus is likely to emphasise the still-strong level of survey indicators, playing down the change of direction. Money trends, by contrast, suggest a further significant cooling over coming months.

Previous posts (e.g. here) argued that the Euroland economy would slow from around spring 2018. Weaker February PMI results are consistent with this forecast. As usual at economic momentum peaks, the consensus is likely to emphasise the still-strong level of survey indicators, playing down the change of direction. Money trends, by contrast, suggest a further significant cooling over coming months.

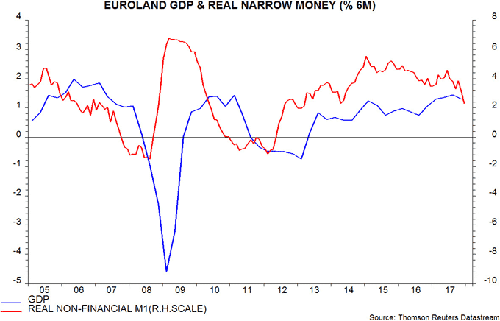

Six-month growth of real narrow money, as measured by non-financial M1 deflated by consumer prices, peaked most recently in June 2017, falling in December to its lowest level since 2014. Allowing for a typical nine-month lead, this signals a likely decline in economic momentum from around March 2018 through September, at least. Two-quarter GDP growth, in fact, may have peaked in the third quarter of 2017, although recent data have tended to be revised upwards – see first chart.

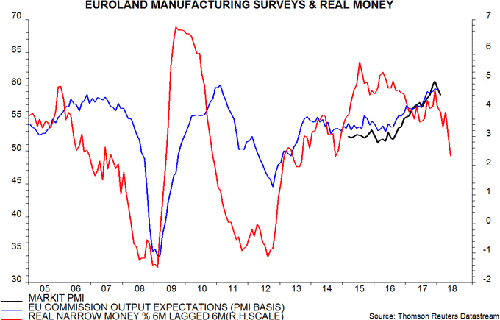

Business surveys lead activity by up to three months, implying that they should reflect monetary trends six months or so later. The second chart shows the manufacturing PMI and output expectations from the EU Commission manufacturing survey, along with six-month real narrow money growth lagged by six months. The survey indicators appear to have peaked on schedule in December, with the February decline in the PMI likely to be echoed by next week’s EU Commission survey. The relationship suggests a further fall in the PMI towards the 50 level by mid-2018.

Why have monetary trends weakened despite ECB President Draghi’s best efforts to delay policy “normalisation”? The view here is that narrow money is demand-determined and influenced importantly by spending intentions, explaining its leading relationship with activity. Sectoral figures show that money holdings of both households and corporations have slowed. Spending intentions may have been dampened by a combination of higher inflation, firmer long-term yields, euro strength, incipient global cooling, Brexit worries and concern that some governments will face financing difficulties as the ECB’s QE backstop is withdrawn.

Diesen Beitrag teilen: