Janus Henderson: UK monetary alarm bells ringing louder

UK monetary trends continued to weaken in February, suggesting deteriorating economic prospects and arguing for the MPC to hold off on plans to raise interest rates.

04.04.2018 | 12:42 Uhr

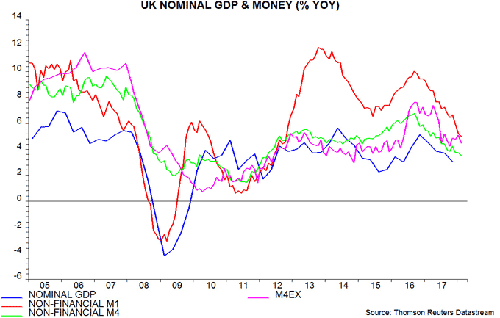

The preferred narrow and broad money aggregates here are non-financial M1 and M4, comprising money holdings of households and private non-financial corporations (PNFCs). Annual growth rates of the two measures fell further to 5.0% and 3.5% respectively in February, the lowest since 2012 and down from peaks of 10.1% and 6.8% in September 2016 – see first chart. The monetary slowdown has been reflected in a decline in annual growth of nominal GDP, to 3.1% in the fourth quarter of 2017. Such a rate of increase, if sustained, would suggest an undershoot of the 2% inflation target over the medium term, assuming trend real economic expansion of around 1.5%.

The preferred narrow and broad money aggregates here are non-financial M1 and M4, comprising money holdings of households and private non-financial corporations (PNFCs). Annual growth rates of the two measures fell further to 5.0% and 3.5% respectively in February, the lowest since 2012 and down from peaks of 10.1% and 6.8% in September 2016 – see first chart. The monetary slowdown has been reflected in a decline in annual growth of nominal GDP, to 3.1% in the fourth quarter of 2017. Such a rate of increase, if sustained, would suggest an undershoot of the 2% inflation target over the medium term, assuming trend real economic expansion of around 1.5%.

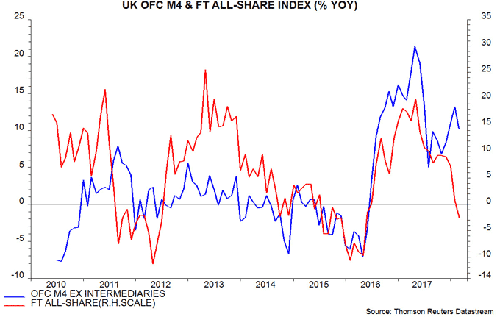

Discussion of UK monetary trends normally focuses on the Bank of England’s M4ex measure, which includes broad money holdings of non-intermediate other financial corporations (OFCs) as well as those of households and PNFCs. Annual growth of M4ex fell to 4.5% in February but is in line with its average over 2013-17, giving a more favourable impression of economic prospects than the non-financial measures. M4ex, however, continues to be inflated by rapid expansion of non-intermediate OFC money holdings, which rose by 10.2% in the latest 12 months and are up by a quarter since February 2016. Such holdings appear to contain little information about near-term spending prospects but have been correlated recently with current (not future) share price movements: market weakness, therefore, suggests a fall in their growth rate – second chart.

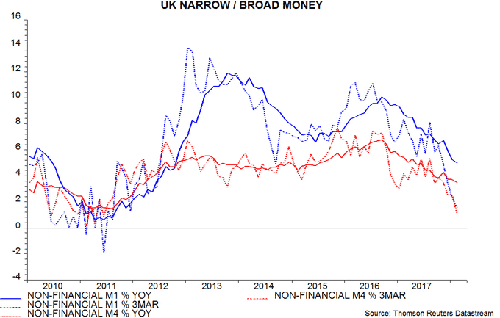

Returning to the non-financial money measures, shorter-term trends have weakened significantly further since the November interest rate increase, signalling a likely further fall in annual growth rates. Non-financial M1 rose at an annualised rate of 1.6% in the three months to February, with non-financial M4 growing by 1.1% – third chart.

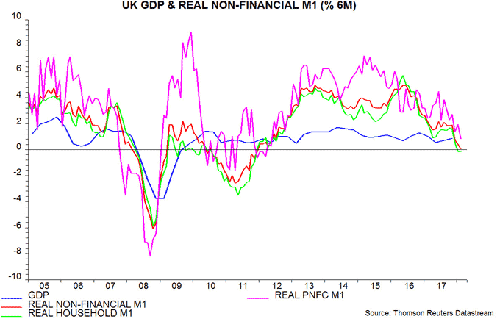

The fourth chart shows the six-month rate of change of real (i.e. deflated by consumer prices) non-financial M1 and household / PNFC components. Aggregate growth fell to just 0.1% in February, with household real M1 in contraction and the PNFC component continuing to slow, consistent with deteriorating prospects for both consumer spending and business investment. These trends, coupled with global monetary weakness discussed in previous posts, suggest that Bank of England and Office for Budget Responsibility forecasts of GDP growth during 2018 (i.e. in the year to the fourth quarter) of 1.8% and 1.4% respectively will be undershot, possibly significantly.

Diesen Beitrag teilen: