BNP Paribas AM: GDP growth in the developed economies: mostly good news

The summer is a good time to review the recent quarterly data for economic growth published in the leading developed economies. In most cases, these are preliminary estimates so they may be subject to adjustment in coming the months.

22.08.2017 | 13:25 Uhr

The data concerned applies to second-quarter growth. An analysis of the behaviour of each component of GDP growth can provide valuable information about future trends.

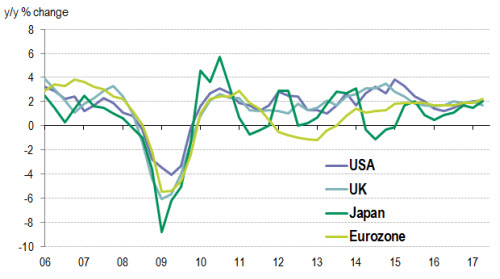

Exhibit 1: The pace of economic growth in is converging at around 2% on an annualised basis in the major developed economies

Source: Bloomberg, BNP Paribas Asset Management, as of 16/08/2017

In the US, GDP grew by an annualised 2.6% in the second quarter, up from a very weak 1.2% in the first quarter. Note that quarterly (non-annualised) GDP expanded by 0.6% and 0.3% respectively. The composition of this growth was positive, with a recovery in consumer spending and a sharp improvement in private non-residential investment. What’s more, inventories were not rebuilt in the second quarter after making a deeply negative contribution in the first quarter, suggesting that this phenomenon will occur in the third quarter and boost activity. Taking into account the bright outlook for productive investment and the still-solid labour market, which should encourage consumers to spend at a time when their confidence is high, US GDP growth is likely to remain dynamic in the second half of the year and to top 2% in 2017 (after average growth of 1.5% in 2016).

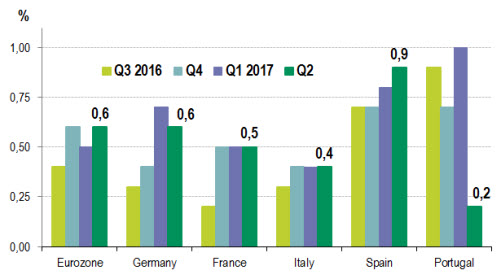

In the eurozone, GDP growth came in at + 0.6% in the second quarter after 0.5% in the first quarter. A detailed breakdown of this growth is not yet available. In France, where GDP grew by 0.5%, (the same rate as during the first quarter), quarterly accounts reveal a slowdown in capital expenditure (from 2.1% to 0.5%) – after receiving an artificial boost in Q1 from the end of the exceptional tax deduction in April – a small improvement in consumer spending (from 0.1% to 0.3%), a sharp increase in exports and a negative contribution by inventories. In Germany, GDP grew by 0.6%, slightly below expectations, but the figures for the preceding quarters were revised up (to +0.7% in Q1), such that year-on-year growth came out at 2.1%, the highest level since the start of 2014.

The carry-over effect (i.e. growth that would be observed in the full year if GDP were to stagnate in the following two quarters) stands at 1.8%. In 2016, GDP grew by 1.9%. The German statistical office reported that second-quarter growth was mainly driven by domestic demand, in particular consumer and public spending. Investment also boosted growth, but the external contribution was negative because of higher imports. Growth in Spain continues to accelerate and remains firm (+0.9%), while Italian GDP grew at the same pace in the first and second quarters (+0.4%). The sharp jump in Dutch growth (+1.5% after +0.6%) was a positive surprise. Economists have significantly revised up their 2017 forecasts for most European countries. This is also true of the IMF, which now expects eurozone growth to reach 1.9%, up by 0.2 of a percentage point from its previous forecast published in the World Economic Outlook last April.

Exhibit 2: Growth remains heterogeneous in the eurozone

Source : Eurostat, BNP Paribas Asset Management, as of 16/08/2017

After confounding forecasts in the second half of 2016, UK growth has slowed since the start of the year, coming in at 0.3% in the second quarter after 0.2% in the first. Activity weakened across industry in the broadest sense, in both the manufacturing sector and construction. The recovery in services, which averted a contraction in GDP, was mainly driven by the retail and hotel segments. The vigour of retail sales should be viewed with caution given that purchasing power has weakened as inflation has accelerated.

In Japan, GDP growth comfortably exceeded expectations at 2% on a year-on-year change and 1% compared with the previous quarter, recording its sixth consecutive improvement. Domestic demand – consumer spending, as well as private and public investment – proved solid, whereas exports fell slightly. However, several leading indicators suggest that caution is appropriate for the rest of the year, in particular regarding capital expenditure, while the consumer spending recovery has been driven by people dipping into their savings as salaries remain stagnant.

Diesen Beitrag teilen: