NN IP: Dollar down

Parallel to the improvement in equity fundamentals, risks have also increased. We observe an improvement in Japanese equity drivers, but we need more evidence to upgrade Japan.

04.09.2017 | 06:34 Uhr

Equity fundamentals have improved in the past week. Macro data came generally in above expectations and earnings momentum has also strengthened, especially in Europe. This is remarkable, given the euro’s strength, and could be an indication that for the time being, the euro headwind is more than compensated by the tailwind of higher global growth expectations.

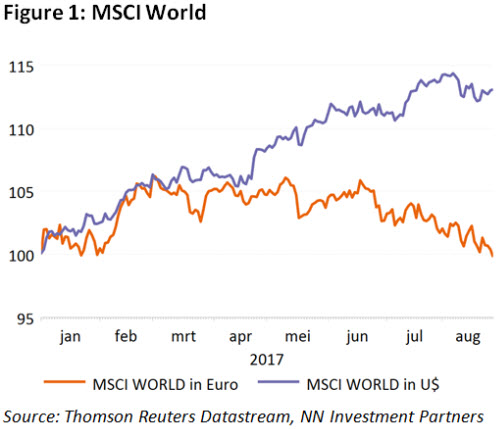

In our view, this euro appreciation also increases the probability of a dovish ECB surprise, as it risks impacting inflation expectations. The direct consequence, however, is the observation that a euro-based investor has not at all enjoyed this fundamental improvement, as year-to-date, the performance of global equities turned negative due to the weakness of foreign currencies.

Unfortunately, parallel to the fundamental improvement, risks have also increased. These are well-telegraphed and are concentrated in the US, where Congress has only 12 joint working days after the summer recess little time to address the debt limit and avoid a government shutdown. In the past, the equity market impact was fairly limited, with the exception of 2011, but that was in a different macro environment with US growth momentum slowing. This time, given Congress’s clumsy functioning, the impact may be bigger as these discussions may divert attention from the plan to reduce taxes. As the health care bill proved, execution risks are high.

And then there is North Korea, which launched another missile that this time crossed Japanese territory. As expected this lead to a rise in the JPY and a drop in bond yields, although the Asian equity market impact has been limited.

This leads us to another topic: The Japanese equity market. On a number of factors, the relative outlook for Japan has improved over the past weeks, even if the improvement was not convincing enough for us to upgrade the region just yet.

First of all, the macro surprises have improved relative to other developed markets. Japan is a key beneficiary of the strengthening of global growth through its sensitivity to the export sector (capital goods, IT hardware and durable consumer goods). However, just as is the case in the rest of the developed work, wage growth is not picking up and inflation expectations are too low, which obliges the BoJ to keep its foot on the accelerator.

The second point is the earnings outlook. Earnings momentum has remained strong and is above the levels observed for European and US. However, the absolute medium-term growth levels are deteriorating. For the current year, Japanese profits are expected to outgrow global profits (15% versus 12.6%) but this will change next year (5.5% versus 9%).

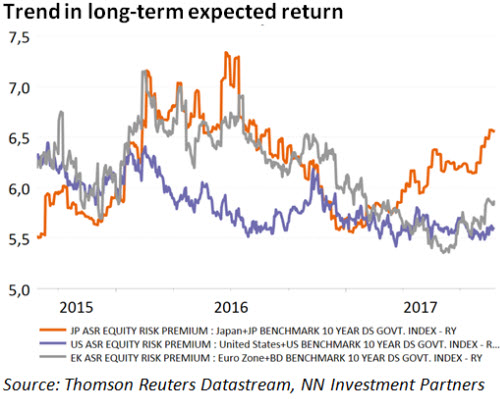

The third element is probably the most convincing: Relative valuations. Japan’s equity risk premium differential to global equities is at least at a 27-year high. One could argue that this is thanks to the low bond yield in Japan, but even if we correct for this, the long-term expected return, defined as risk premium plus risk free bond yield, is almost 100bp higher than in the US.

Similarly, if we compare the return on equity with the price-to-book, then Japan again comes out on top. It has a comparable ROE to Eurozone, but it comes at a substantially lower price-to-book.

The negative correlation with the USD/JPY remains an important factor for Japanese equities. However, we recently saw that this USD-sensitivity has decreased. The euro’s strong appreciation has probably compensated for the USD’s fall. Of course, Japan also depends on international monetary policies. In view of inflation undershooting the target in the Eurozone and the US, we cannot exclude a dovish surprise from the ECB or even the Fed. This could make the JPY stronger against these two currencies and hence weigh on market performance.

A final point is the political situation. For some time, Abe’s approval ratings were at dangerously low levels. Since his cabinet reshuffle in early August, the trend looks to be reversed with his approval rate recovering by 4 percentage points to 46%. This also comforts the position of Kuroda as governor of the BoJ.

All in all, drivers have shown an improvement but we would like to see some confirmation of these drivers’ persistence.

Diesen Beitrag teilen: