Janus Henderson: G7 money surge suggesting too-loose policies

Six-month growth of global real narrow money* continued to strengthen in June, signalling a likely pick-up in economic momentum in late 2017/early 2018, after a modest near-term slowdown. Monetary acceleration suggests that major central banks are falling behind and will be forced to tighten policies significantly as economic growth and inflation rebound.

10.08.2017 | 15:02 Uhr

(Foto: Simon Ward)

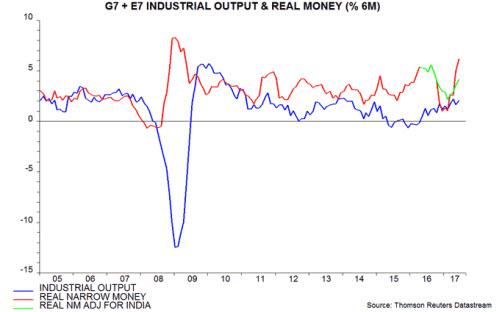

Six-month growth of global (i.e. G7 plus emerging E7) real narrow money, adjusted for Indian demonetisation, bottomed in February 2017, rising for a fourth consecutive month in June to its highest since September 2016. Allowing for an average nine-month lead, this suggests that six-month industrial output growth will strengthen from around November – see first chart.

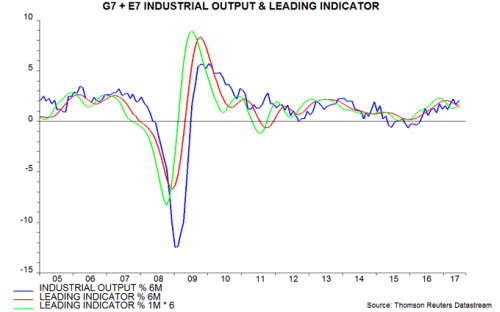

Economic momentum is likely to moderate shorter term, reflecting a fall in real narrow money growth between August 2016 and February. This is also the message from the global leading indicator tracked here: it typically leads by four to five months and its six-month growth declined again in June**. The one-month change in the indicator, however, rose for a second month, suggesting an imminent turn in the six-month measure – second chart. Such a turn would confirm the signal of economic reacceleration from late 2017 from monetary trends.

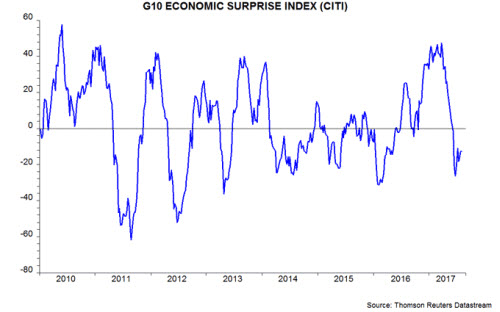

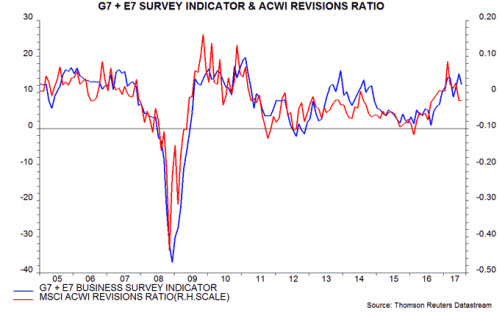

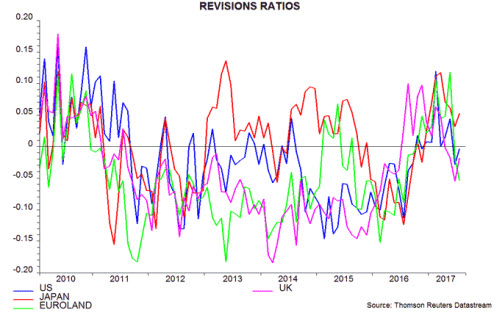

Coincident economic news remains mostly solid but is cooling at the margin. The Citigroup G10 economic surprise index turned significantly negative in June and has remained weak – third chart. The global manufacturing business survey indicator tracked here ticked down in July, while the MSCI All-Country World Index earnings revisions ratio was negative for a second month – fourth chart. The Euroland ratio has reversed particularly sharply, partly reflecting the strong euro, consistent with the expectation here of weaker economic news – fifth chart.

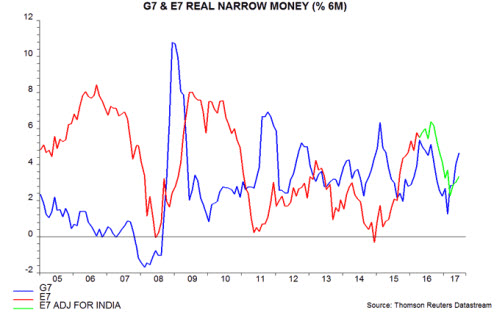

The pick-up in global real narrow money growth has been led by the G7 and the US in particular. G7 real money growth is now well above the India-adjusted E7 level, questioning the sustainability of recent EM asset outperformance – sixth chart. E7 real money growth is respectable in absolute terms but has been held back by moderating – though still solid – Chinese expansion and a contraction in Mexico following recent significant monetary policy tightening.

*Narrow money = currency in circulation plus demand / overnight deposits. Financial sector holdings excluded where possible. Real = deflated by consumer prices, seasonally adjusted.

**June estimate based on partial data.

Diesen Beitrag teilen: