Henderson: Sterling not overvalued before Brexit vote

Brexit-supporting economists argue that the referendum result hastened a fall in the pound that was inevitable and will ultimately prove beneficial. Such claims are dubious.

11.10.2016 | 14:20 Uhr

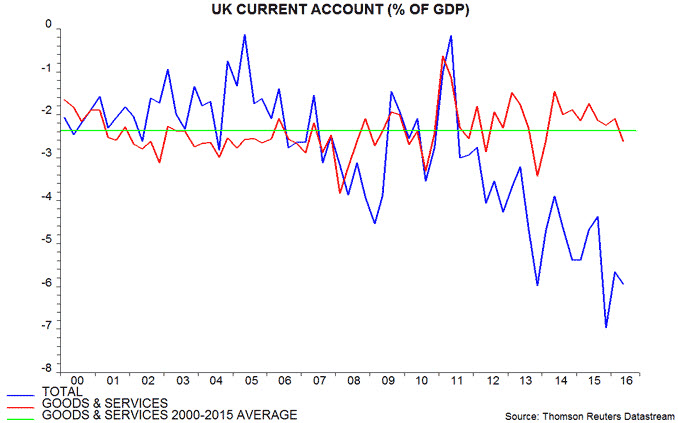

The Brexit supporters cite the large current account deficit – equivalent to 5.9% of GDP in the second quarter of 2016 – as evidence that the pound was significantly overvalued. The trade deficit in goods and services, however, was 2.6% of GDP in the second quarter, close to its average of 2.4% between 2000 and 2015. It has been trendless in recent years despite relatively strong UK domestic demand growth – see first chart.

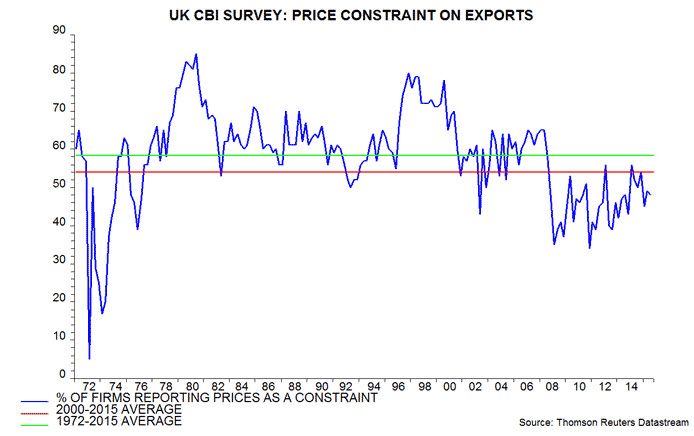

Business survey evidence refutes the claim that the pre-referendum level of the exchange rate was limiting export performance. The percentage of CBI industrial firms citing pricing as a constraint on exports stood at 49% in April, below a 2000-15 average of 54%. The long-term average (since 1972) of this series is 58% – second chart.

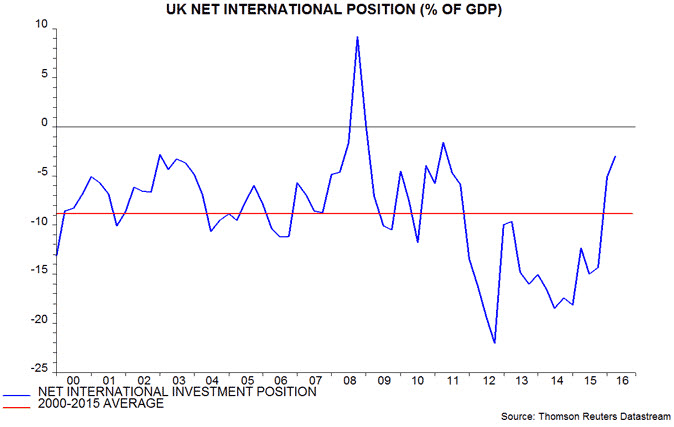

The rise in the current account shortfall has been driven by a move from surplus to deficit in the investment income balance. This move, however, has reflected a change in the form of the return received on foreign assets from income to capital gain. The cumulative capital gain on the net international investment position in recent years has exceeded not only the income deficit but also the overall current account shortfall. The net investment position (i.e. external assets minus liabilities) stood at -5.1% of GDP at the end of the first quarter (before the referendum) versus a 2000-15 average of -8.8% – third chart.

An alternative view is that the fall in the pound was not inevitable but has been the result of international investors revising down their assessment of the equilibrium value of the exchange rate in response to 1) the UK opting for inferior trading arrangements with its largest export market and 2) post-referendum monetary and fiscal loosening. The MPC bears significant responsibility – cutting rates and launching more QE when broad money is growing at a double-digit pace* is a recipe for a weak currency.

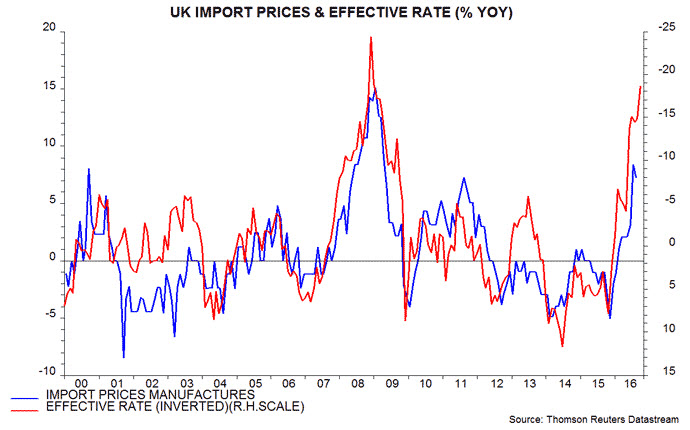

Monetary trends were signalling a rise in inflation in 2017 well before the Brexit vote. Sterling’s slide will accelerate the pick-up as import prices surge – fourth chart. CPI and RPI inflation are expected here to rise above 3% and 4% respectively during the course of next year. Will Brexiters comfortable with the pound’s decline also defend these increases as inevitable and necessary?

*M4ex rose at an annualised rate of 11.3% in the four months to August.

Die Wertentwicklung in der Vergangenheit ist kein zuverlässiger Indikator für die künftige Wertentwicklung. Alle Performance-Angaben beinhalten Erträge und Kapitalgewinne bzw. -verluste, aber keine wiederkehrenden Gebühren oder sonstigen Ausgaben des Fond.

Die Informationen in diesem Artikel stellen keine Anlageberatung dar.

Diesen Beitrag teilen: