Schroders: Climate change and the global economy: regional effects

In the third of a series of four articles, Keith Wade and Marcus Jennings discuss how climate change will affect developed and developing countries differently.

27.07.2015 | 15:35 Uhr

The burden of climate change will be felt most by the developing world

The effects of climate change will not be uniformly distributed across the globe and there are likely to be winners and losers as the planet warms. Applying a broad brush to climate effects, developing countries are more likely to disproportionately experience the negative effects of global warming. Not only do many developing countries have naturally warmer climates than those in the developed world, they also rely more heavily on climate sensitive sectors such as agriculture, forestry and tourism. As temperatures rise further, regions such as Africa will face declining crop yields and will struggle to produce sufficient food for domestic consumption, whilst their major exports will likely fall in volume. This effect will be made worse for these regions if developed countries are able to offset the fall in agricultural output with new sources, potentially from their own domestic economies as their land becomes more suitable for growing crops. Developing countries may also be less likely to create drought resistant harvests given the lack of research funding.

The increased frequency and severity of extreme weather will weigh on government budgets. The aftermath of natural disasters often falls on authorities who are forced to spend vast amounts on clear-up operations and healthcare costs that come with experiencing extreme weather. Revenue reductions may also be experienced by countries heavily dependent on tourism or on selling fishing rights, for example.

The effects on the developing world are two-fold. Firstly, as developed countries face an increasing strain on domestic budgets, fewer resources in the form of aid and economic development funds will flow to developing countries. Secondly, the governments of these nations will be forced to channel resources away from productive and growth-enhancing projects towards countering the costs of extreme weather. Such effects will damage near-term growth prospects. Furthermore, developing countries are likely to have less capacity to rebuild. The time required to recover from natural disasters will be prolonged and if longer than the frequency in which such disasters occur, many developing economies could remain in a constant state of reconstruction.

Parts of Africa and Asia most at risk

Highly vulnerable regions in the emerging world include Sub-Saharan Africa and South and South East Asia, according to the World Bank. In South Asia, cities such as Kolkata and Mumbai will face increased flooding, warming temperatures and intense cyclones. Loss of snow melt from the Himalayas will also reduce the flow of water into the Indus Ganges and Brahmaputra basins. Meanwhile in South East Asia, Vietnam's Mekong Delta, which produces most of the rice, is especially vulnerable to rising sea levels. For Sub-Saharan Africa, food security will be a major challenge due to droughts and shifts in rainfall.

Many developing nations are situated in low latitude countries and it is estimated that 80% of the damage from climate change may be concentrated in these areas. In contrast, northerly regions such as Canada, Russia and Scandinavia, may enjoy a net benefit from modest levels of warming. Higher agricultural yields, lower heating requirements and lower winter mortality rates are a handful of economic benefits climate change may bring, although these benefits may diminish as warming continues.

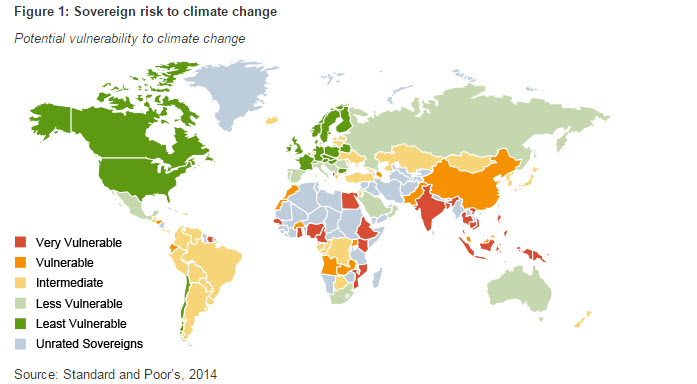

The prediction that developing countries will be disproportionately affected is reinforced by Standard and Poor's research on the influence climate change will have on sovereign risk. Recognising that climate change is a global mega-trend impacting sovereign risk through economic, fiscal and external performance, they find that lower-rated sovereigns appear most exposed. They assess sovereign vulnerability on three measures: share of the population living in coastal areas below five metres of altitude, the share of agriculture in national GDP and a country score from the "vulnerability index" compiled by the Notre Dame University Global Adaption Index. Such an index measures the degree to which a system is susceptible to, and unable to cope with, adverse effects of climate change. Based on these measures we can interpret the results in part as the susceptibility of an economy to climate change. Figure 1 below summarises the results on a world map. In line with much of the economic literature, many developing nations appear most vulnerable to climate change during the remainder of the current century.

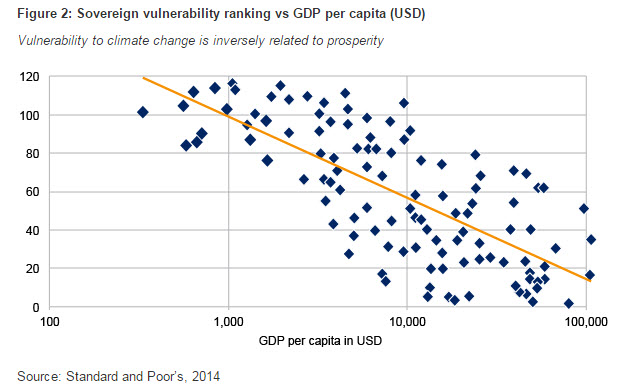

Alternatively, Figure 2 below expresses this trend of higher vulnerability amongst poorer countries by plotting the overall vulnerability ranking against GDP per capita for each country.

UK should fare better than developed peers

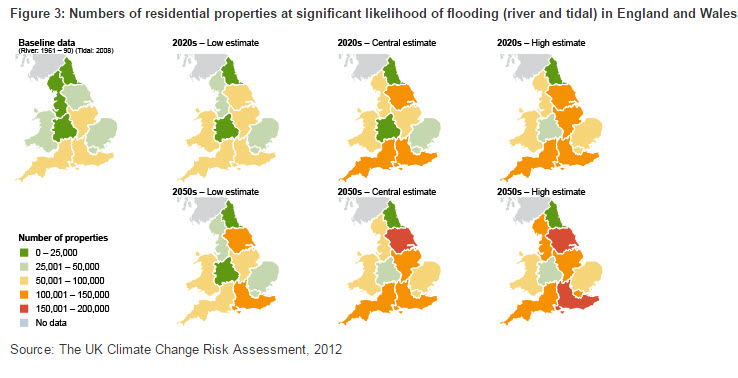

In the UK, the average temperature is now 1°C higher that it was 100 years ago and 0.5°C higher than it was in the 1970s. As a higher latitude country, it is believed that the UK will fare better than many developing nations as global warming progresses. That is not to say the nation will escape the costs of climate change - particularly given its significant coastline where rising sea levels pose an obvious threat. According to Stern, estimates of the cost of floods to the UK economy as a result of 3°C - 4°C of warming are in the region of 0.2% - 0.4% of GDP annually by the middle of the century, if flood management efforts are not strengthened. In England, the south and parts of Yorkshire and Humberside are forecast to experience the greatest impact from flooding by 2050 as shown by Figure 3.

Aside from increased flooding, water availability will become progressively more constrained and droughts more frequent. Milder winters and the associated decline in cold-related mortality rates will be countered by a greater prevalence and severity of heat waves, bringing with it a higher number of heat-related mortalities. Finally, with the agricultural sector contributing approximately just 0.6% of GDP, the benefits of longer growing seasons will be marginal to the economy.

Climate change may also indirectly affect the UK economy through global supply chains. The UK may both export to and import from climate-sensitive countries. The subsequent influence of climate change in these economies may feed through to the domestic economy through lower demand for exports or higher prices of imports for example.

Diesen Beitrag teilen: