BNP Paribas AM: Equity volatility is back

Protectionism on the rise: the Trump administration caught markets off guard with new tariffs on Chinese goods; Experts from BNP Paribas believe the probability of a severe escalation remains small.

09.04.2018 | 13:33 Uhr

The first quarter of 2018 started with an acceleration of the positive equity trend, low volatility as well as rising yields seen in 2017. This lasted until the end of January when financial markets sold off amid concerns over inflation that sparked a technical correction. Investors betting on prolonged low volatility levels were hit hard as the VIX index spiked higher. The index is now hovering at around 20, twice the 2017 levels. The macroeconomic fundamentals globally have remained robust and they have supported a tentative equity rebound.

However, this shock unearthed additional concerns making the equity market more sensitive to volatility.

First, US President Trump announced tariffs on steel and aluminium and unveiled a plan to tax Chinese goods over intellectual property rights breaches. As we pointed out in our Spotlight report on protectionism, this could hinder the globalisation dynamics and hurt the global economy by derailing global supply chains, especially if this escalates into a fully blown war.

Second, the tech sector had a bumpy March. It had been contributing significantly to global equity performance over the past few quarters. Protectionism concerns struck a first dent in this heavily-globalised sector. A further punch came from allegations that Facebook had misused private data. Concerns over the risk of more stringent regulation hurt shares in the social network before spreading to other tech companies such as Alphabet (Google’s parent company).

Finally, activity data started to roll over including PMI indicators, especially in Europe. Market participants had expected stronger numbers, so the surprise weakness hurt financial assets. Notwithstanding these weaker indicators and the short-term market reactions, absolute data levels have remained high and firmly anchored in expansionary territory. Therefore we remain comfortable with our Goldilocks scenario of strong growth and muted inflation.

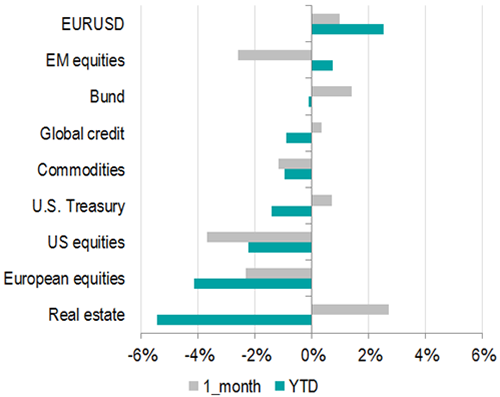

Looking at asset performance over Q1 2018, equities are the main laggards despite January’s strong performance. UK and German equities are down by 8.2% and 6.4%, respectively (in local currency terms). The US S&P 500 lost a mere 1.2% over the quarter, but it is down by 8.1% since its late January peak.

So far, emerging markets have been affected less by the turbulence. Brazilian and Russian equities did best with +11.7% and +7.6%, respectively. This was helped by a weak US dollar which continued to depreciate moderately despite the continued Fed rate-rising cycle.

On the duration side, the quarter started with rising yields amid concerns over inflation and a potential acceleration in Fed policy tightening. However, markets switched to risk-off mode in February and March, which benefited haven assets such as US Treasuries and German Bunds. US and German 10-year bonds rallied by 21bp and 27bp respectively from their intra-quarter peaks.

Gold investors enjoyed the precious metal’s haven status: gold has risen by 1.7% Ytd. On the other hand, industrial metals such as copper and iron ore did poorly amid steady supply and cautious investor sentiment over the economic cycle and the potential impact of a trade war on Chinese demand. Crude oil had a volatile quarter, but WTI ended up by7 7.5%, pushed higher by a tougher US stance towards Iran.

Figure 1: Partial rebound for risk assets, but bonds and rate-sensitive assets lag

(Source: Bloomberg, BNPP AM, as of 2 April 2018)

Higher inflation prospects spooked markets

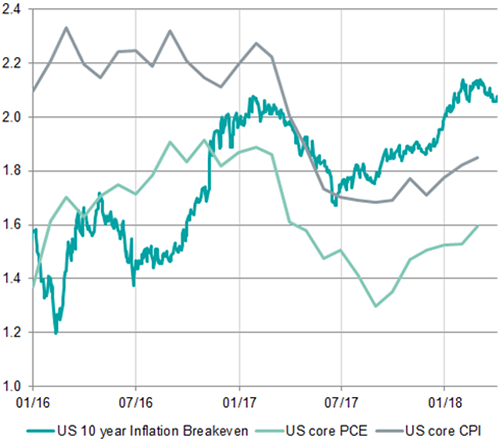

The main concern in investors’ minds at the beginning of the year was the prospect of higher inflation, especially in the US. Market participants knew that any abrupt change towards reduced central bank accommodation could disrupt the low-volatility environment of the last few years. So far, the US Fed has managed to withdraw stimulus very gradually, largely because inflation, notably core inflation, has remained low. If markets take the view that inflation is on the rise, the low-volatility and risk-friendly environment could sour.

That is exactly what happened in early February. US breakeven inflation (BEI) had been rising since mid-December 2017, but it was strong hourly earnings data that tipped the balance. This lead to an abrupt market correction that was accelerated by strategies that hinged on a low-volatility environment. Some say perception is reality in markets: US core inflation (both on the CPI and PCE metrics) did increase over the same period, but it remains well below the Fed’s 2% target (Figure 2).

Figure 2: US BEI rose in Q1, while core inflation remained muted

(Source: Bloomberg, BNPP AM, as of 2 April 2018)

Diesen Beitrag teilen: