Janus Henderson: Tech titans’ results support the ‘technology flywheel’

Global technology portfolio managers Alison Porter, Graeme Clark and Richard Clode, discuss how recent earnings announcements by Apple, Amazon, Alphabet (Google), Facebook and Microsoft highlight the team’s view that the technology sector continues to take share.

22.02.2018 | 12:45 Uhr

Key takeaways:

• Tech has continued to outperform broader equities in 2018 so far (1).

• US tax reform on repatriation of overseas cash is facilitating an acceleration in investment.

• The technology sector has the strongest balance sheets and free cash flow among the global sectors (2).

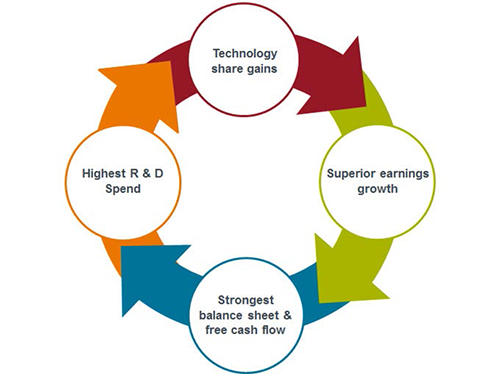

Technology stocks have continued to outpace broader equity markets in early 20181. Combined, global tech titans Apple, Amazon, Alphabet, Facebook and Microsoft currently have a market capitalisation value of around $3.6 trillion and a net cash balance of just over $365bn. The five companies’ latest quarterly earnings reports epitomise a virtuous circle of cash generation, investment and share gains. This is the result of the accelerating ‘technology flywheel’ that is increasing the sector’s momentum and ability to take share (see Chart 1).

Chart 1: The ‘technology flywheel’

(Source: Janus Henderson Investors.)

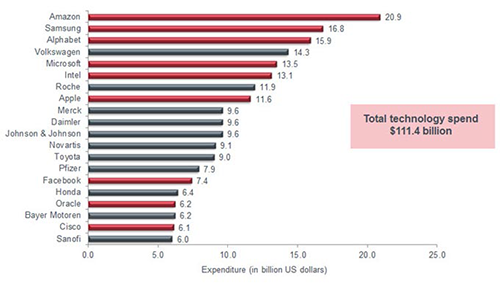

Tech companies are among the heaviest investors in R&D

Technology has accounted for the vast majority of earnings growth of the S&P500 Index in the last ten years (3). The cash being generated by these companies facilitates further reinvestment in new technologies. Of the top 20 global spenders on R&D (research & development) in 2017, nine were technology companies (see Chart 2). This high level of reinvestment is propelling new products and future growth, driving the ‘technology flywheel’.

Chart 2: Technology companies represent 9 out of top 20 global spenders on R&D in 2017

(Source: Janus Henderson Investors, Bloomberg, as at 31 December 2017.)

New user interfaces and products are driving AI adoption

New product developments and the exponential growth in data generated are pushing the tech sector towards the fourth wave of computing - artificial intelligence (AI). New user interfaces such as 3D sensing (capturing object shapes through 3D laser scanning), augmented reality and voice have become more evident through 2017, with the iPhone X and home assistants from Amazon and Google featuring heavily on Christmas wish lists. Apple sold 77.3m iPhones in Q4 2017 while Google and Amazon each sold “tens of millions” of their virtual assistant devices in 2017.

Investing in next generation infrastructure now

These companies are at the forefront of investments in next generation infrastructure to support the move towards artificial intelligence. Next generation infrastructure includes the shift to “cloud infrastructure” - large industrial scale computing and storage that enables cheap fast compute power and access to machine learning. Amazon Web Services (AWS), Microsoft Azure and Google’s cloud platform are leading the way in the moving of IT workloads from on premise to public cloud:

In the fourth quarter of 2017 the largest of the public cloud vendors, AWS saw sales grow over 45% and announced several new cloud agreements with companies such as Expedia, Walt Disney, and Honeywell. AWS already counts government agencies such as the Central Intelligence Agency (CIA) and Federal Bureau of Investigation (FBI) in the US and the National Health Service (NHS) in the UK among its clients.

Microsoft’s Azure cloud segment announced growth of over 98% over the quarter ended 31 December 2017. Google reported that its cloud platform had reached revenues of over $1bn in Q4 2017.

Building cloud infrastructure is highly capital intensive and the cost is a barrier to entry to less well-resourced tech companies – indeed HP Enterprise and IBM have fallen by the wayside in the cloud race. High barriers to entry are translating into high operating margins at scale.

Tech titans – challenges and opportunities

Apple

While unit sales of the new iPhone moderately disappointed, the average selling price surged with the launch of the new premium-priced iPhone X. Apple and its investors are increasingly focused on the company’s active installed base of 1.3bn devices and the potential to monetise those accounts. If Apple’s services division was considered a single entity it would be the ninth largest internet company in the world. As the smartphone market matures and the replacement cycle for iPhones is elongating the challenge is for Apple to grow the services division to drive growth.

The reform of the US tax system is beneficial to Apple as it has $163bn of net cash held overseas. Tax reform will allow Apple easier access to this cash and could be the catalyst to spur M&A (merger & acquisition) activity to help boost its services division. The company announced that it would be comfortable with a close to zero net cash balance, opening the door to significant shareholder returns in the form of increased dividends and share buybacks, which provides downside support during this period of business transition.

Alphabet (formerly Google)

Alphabet recorded sales growth of 24% year-on-year in Q42017. Its Google core search platform continues to be the main driver of Alphabet’s earnings. While search volume continues to be strong the challenge for Alphabet is that the cost of this search volume is increasing. Traffic acquisition costs (TAC), on mobile are higher than on desktop with Alphabet having to make payments to partners (such as Apple) and this inhibits operating leverage.

The Google search engine is a sophisticated AI tool and Alphabet has been finding new areas to leverage this expertise into a wide range of applications such as its cloud platform, YouTube, and in its ‘other bets’ (areas outside its core search business divisions), which includes healthcare venture Verily and Waymo, one of the leader in autonomous driving. We believe that the pace of increase in TAC costs will abate in the second half of 2018 and that the company’s large cash pile will facilitate shareholder returns and M&A. However, Alphabet will undoubtedly face ongoing regulatory scrutiny this year, from both the European Union and in the US on its dominance in online advertising.

Facebook

Despite concerns over user engagement and changes to the core newsfeed, Facebook reported revenue up 47% year-on-year in the fourth quarter. The company is focusing more on community and interactions − quality over quantity of time, which lends itself well to taking share in the growing global social media advertising market. Facebook has a number of other growth drivers, with its positioning in India (now the largest market for users) as well as growth from Instagram and WhatsApp. While these are likely to driver another year of stellar earnings growth, the valuation of the company will be challenged if Facebook is unable to maintain engagement levels on its core newsfeed product in the US, which remains the most lucrative advertising market in the world.

Amazon

Amazon best exemplifies the ‘technology flywheel’ in action. In 2017 the company was the global leader in R&D spend. Amazon recorded full-year revenue of $177.9bn in 2017 − an impressive acceleration with Q4 2017 sales growth of 38.5%. Amazon is increasingly viewed as a brand, a portfolio of companies and services in e-commerce, advertising, media, logistics, IT infrastructure and more recently healthcare. While its US retail business continues to grow rapidly, Amazon’s international growth has been more muted. Cash is typically reinvested quickly enabling investors to get a rare glimpse of its potential long-term profitability. As an investor in Amazon we appreciate that traditional short-term earnings metrics do not capture the value of future growth potential. The challenge for Amazon in 2018 may be that rising interest rates make investors focus more closely on short-term profitability than long-term growth potential.

Tech sector and recent US tax reform

US tax reform is facilitating easier repatriation of cash from overseas. Tech companies’ and its investors will benefit from this given their global earnings base and the large cash balances held offshore particularly by the sector’s giants. We believe this will translate not only into higher levels of capital expenditure and R&D but also increased shareholder return in the form of buybacks and/or dividends.

Many of the tech titans have recently announced that the tax reforms are enabling them to increase investment in the US, create more jobs and train workers:

Apple pledged to contribute $350bn to the US economy in the next five years through $5bn in an advanced manufacturing fund and the creation of 20,000 jobs.

Amazon has said it will hire more than 100,000 staff in the next 18 months.

Alphabet will open five new US data centres in 2018.

Facebook to double its capital expenditure to at least $14bn in 2018.

Conclusion

Notes:

1) As measured by MSCI ACWI Information Technology Index vs MSCI World Index total returns in US dollars, 31 December 2017 to 19 February 2018. Please note past performance is not an indicator of future performance.

2) Source: Credit Suisse as at 22 January 2018. MSCI World Sector indices excluding financials. Refers to net cash as % of total market capitalisation. Free cash flow measured by EV/FCF yield ie Enterprise Value/Free Cash Flow: the reciprocal of Trailing EV)/ Trailing FCF).

Diesen Beitrag teilen: