Janus Henderson Investors: Kein Wachstum, keine Inflation – ist MMT die Lösung?

John Pattullo, Co-Head of Strategic Fixed Income sowie Fondsmanager der Strategien Strategic Income und Global Dividend Income bei Janus Henderson Investors, sieht die globale Finanzkrise von 2008 nach wie vor nicht als beendet an, denn die meisten Länder haben heute mehr Schulden als vor 11 Jahren zu Beginn der Krise.

19.06.2019 | 09:20 Uhr

Nachdem

es durch QE nicht gelungen ist, nachhaltiges Wachstum zu generieren

oder die Inflationsrate zu erhöhen, verlagern sich die Bemühungen nun

auf verschiedene Formen der Fiskalpolitik. Pattullos Argumentation

zufolge verspricht nur eine aufeinander abgestimmte Verbindung von

Geldpolitik, Steuer- und Strukturreformen Erfolg.

Er stellt dazu Richard Koos Theorie der „Bilanzrezession“ den Positionen der Modern Monetary Theory gegenüber, insbesondere Koos Aussage, dass die Befürworter von MMT Recht haben, wenn sie argumentieren, dass es steuerliche Anreize braucht, um den Überschuss an Ersparnissen des Privatsektors aufzufangen - das jedoch nicht bedeute, dass es die Zentralbank selbst sein müsse, die den Stimulus direkt finanziert.

What crisis?

"Do you remember the Great Financial Crisis?“ Ahh — you mean the one we are still in…

It

is rather amusing that we sometimes get asked the above question. We

need to remind some clients that we are very much still in the crisis.

The

crisis happened for a number of reasons but primarily because of the

enormous amounts of debt raised by households, corporations and

governments. Hence, a lot of the economic ‘growth’ was financed by

increasing debt in an unsustainable way. Remember the ‘Great

Moderation’?1 Hmm…

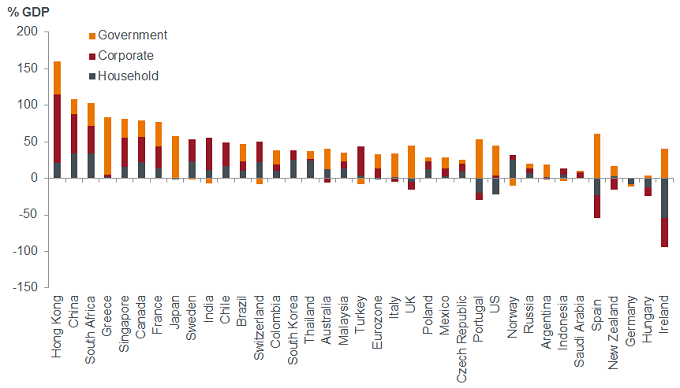

Eleven years on, as the chart

demonstrates, the vast majority of countries have more debt than before

the crisis began — a few have managed to partially reduce their debt.

So, how on earth can the crisis be over?

Debt loads higher than pre-crisis

Source:

Thomson Reuters Datastream, BIS, Janus Henderson Investors, change in

aggregate debt, 2008 versus 2018, annual, as at 31 December 2018

Note: Aggregates for household, corporate and government

There

are no easy solutions to reducing too much debt. A number of options

are available, such as growth and inflation (which are hard to come by),

austerity, default and/or financial repression2 (more on this later). But the not so distant past may have lessons that can help.

Japanification alert!

It was back in 2011 that we started talking about Richard Koo’s balance sheet recession3

thesis. It is extraordinary how reading one book (The Holy Grail of

Macroeconomics: Lessons from Japan’s Great Recession, 2009) can

completely change your view on economics and the bond markets.

In

2009, he prophetically forecast that Europe would turn Japanese. We

have talked about this for years but it is only recently that our inbox

has become full of ‘Japanification’ articles on Europe. This backdrop

explains why we have maintained a much longer duration in our portfolios

for much of the time compared to many in our peer group, given our

rejection of mainstream conventional economics.

Rather bizarrely,

we are pleased to still get some push back on our views from the

(older) part of our client base, which means there is still money to be

made in bonds. Some of our clients remain short of duration or have

tried their luck diversifying into alternatives, away from quality, long

duration bonds. Most though, who are younger than me (49 in May —

urgh!), agree with our disinflationary outlook.

We feel that the

long-term secular drivers such as demographics, technology, excessive

debt and low productivity, will dominate and lead to lower global bond

yields. We doubt whether we can sustainably breakout into higher

inflation and growth but it does not mean that politicians, with a

democratic mandate, could try something completely different (more on

this later).

Wot no growth, wot no inflation?

Here’s the title slide from our 2013 UK New Year Conference presentation.

Our 2013 presentation cover — still relevant today?

Source: Janus Henderson Investors, January 2013

In

the presentation we highlighted how small the money multiplier could be

compared to the fiscal multiplier in a severely depressed economy. Our

message was that fiscal policy tools should be employed to restore

growth but there was no political will at the time for such measures.

The

Global Financial Crisis was no ordinary recession; this was a ‘balance

sheet’ recession whereby individuals and corporates changed their

behaviour towards borrowing and spending after the trauma of

experiencing negative equity. In such circumstances, lowering interest

rates does no good and policies focusing heavily on the monetary side

may not be effective, as we have seen.

Monetary policy broadly

became independent in the 1990s (in many countries) with the aim of

taking politics out of the business cycle. Keynesian fiscal expansion

was pretty much dismissed by conventional economists during this period

as being ineffective. As the dogmatic Maastricht Treaty removed the

possibility of fiscal expansion in Europe, the ‘one-clubbed golfer’ of

independent interest rates seemed to be the only policy tool.

While

it is true that quantitative easing (QE) has massively expanded the

monetary base, as Mr Koo demonstrates, it completely decoupled from the

growth in bank lending and money supply. We have definitely created

asset price inflation in Wall Street with no ‘trickle down’ effect into

Main Street. The palliative needed was something along the Koo Theory.

Koo Theory

In ‘Koo Theory’, the government needs to borrow all the

private sector surplus and redistribute via fiscal policy to stop the

economy shrinking into oblivion. This very much chimes with the secular

stagnation4/excessive savings hypothesis of American

economist, Larry Summers. Unfortunately, our policymakers do not

subscribe to the Koo thesis. If all this surplus is not redistributed

you get a deficit of demand and deflation — anyone mention Europe?

Why

then was monetary policy not combined with fiscal policy? Surely, they

should be complementary and not treated as substitutes. Italy, for

example, would have welcomed (still welcomes) a massive fiscal expansion

(even though the Maastricht Treaty prevents it). As Koo points out, you

need structural reform before a fiscal expansion otherwise it will

fail. Indeed, he said that 80% of the necessary change is structural

reform, followed by fiscal expansion. Note that this third arrow of

structural reform was never delivered in Japan.

Somewhat

ironically, the inequality brought about by QE has led to the populist

backlash in developed economies as well as calls for Modern Monetary

Theory (MMT)5/fiscal expansion — but let’s not confuse the two for now.

Anyway, what’s all this MMT chat?

Modern

Monetary Theory is really just a politicisation of fiscal spending with

unlimited constraint. No one constrained the British and the American

fiscal expansion in World War II (WW2); tanks and warships were needed,

so they were made. The idea was that governments spend as much as needed

to achieve the desired outcome and worry about financing the deficit at

a later stage.

So, after the abject failure of QE to generate

any sustainable growth or inflation, the political dial has now turned

to fiscal policy. Now, governments are always keen to inflate away their

debt — by running inflation higher than the nominal yield on the debt

that they issue. This policy is called financial repression and is one

way to deleverage an economy (reduce debt). Interestingly, the reduction

in debt generally happens via growth in the economy (ie, higher GDP),

which reduces the debt as a percentage of GDP but rarely a reduction in

the absolute level of debt.

Since only very low inflation could

be generated, interest rates had to go even lower to try to reflate the

economies but also to enable negative real interest rates (to repress

you and I!). Rest assured, further financial repression is both required

and necessary to reduce global debt levels but the current rate of

progress is too slow.

Times are different now?

The

economic downturn that we are in is not going to recover to previously

normal levels. Given poor demographics and productivity, the future

trend rate of growth in both the US and UK is around 1.5-1.75%. We are

in a different regime after the ‘heart attack’ of 2008 — one of low

growth, low inflation and increasing financial repression. As mentioned

earlier, Richard Koo has called for a wartime response on the fiscal

side as this is wartime economics but currently nobody has the political

mandate to justify such a response, although things are changing fast.

So this brings us back to MMT

The

theory that a government cannot default on its debts if those debts

were issued in its own currency is not new. There is also a vast amount

of economic literature on whether fiscal deficits matter. Still, this is

certainty getting a big (political) push nowadays.

It

is hard to argue that significant expansion in infrastructure, housing,

technology, transport and education would not boost the economy and,

would surely have a much bigger multiplier effect than QE. The tricky

bit is how it is financed and the potential repression (redistribution)

of wealth that goes with it. Could such a stimulus offset the long-term

secular drivers? Possibly, but we are not convinced.

In Koo’s

words, “MMT proponents are correct in arguing we need enough fiscal

stimuli to absorb the private sector savings surplus. However, this does

not necessarily mean we need the central bank to directly finance the

stimulus”*. This is a key point in the MMT debate, which many people

confuse — the stimulus should be funded from a private sector savings

surplus not by the central bank.*Nomura, Richard Koo, research paper titled: “MMT and the EU’s growing sense of crisis”, 23 April 2019

MMT fears — UK to be a test case?

What if the UK tried a massive Corbyn’s ‘People’s QE’6

programme? Well, it depends on its credibility and how it is financed.

This could be accompanied by rising gilt yields, inflation and a

sterling crisis — or possibly not. Bondholders would be repressed as

inflation took off. Yield curves could steepen aggressively while the

rich would be taxed heavily. Could the Bank of England lose its

independence? We feel this scenario is less likely, but that does not

mean we are not worried about markets worrying about it.

A more subtle, more palatable, approach could involve the central bank anchoring bond yields at a low (repressing) level set by law. The government could then issue endless bonds to the central bank to finance the fiscal expansion. This would be a more controlled expansion with some repression. It would probably involve capital controls (to stop capital escaping overseas) and financial regulation, eventually forcing financial institutions to be forced buyers of gilts once the central bank is full!

Neither sounds great for bondholders; but again, and as always, we turn to Japan where they still have not conjured up any meaningful or sustainable growth or inflation. One of their main impediments is the combination of abysmal demographics and lack of structural reform.

America and China have had some success with fiscal expansions, whereas Greece, Cyprus and Iceland have already had several degrees of repression and indeed capital controls. Many forget that UK citizens were repressed for decades post WW2 under varying forms of legislation. France, also massively reduced large government borrowing levels after WW2 by running inflation (at times over 20%) but keeping bond yields at around 6% by law. UK citizens are currently being repressed with bond yields at 1% but inflation at 2%.

So what will work?

We have sympathy for fiscal, monetary and structural reform — working together — but say no to MMT if badly financed. It is the combination of these factors that is key.

Fiscal policy can be effective if credibly financed and used at the right time in the cycle. Further, it must be invested and not consumed. Debate continues about the financing angle with regards to MMT, much of which is political and highly ideological (the heterodox school of economics), to which this is no definitive answer. Politics may also throw a spanner in the works as to the effectiveness (or credible financing) of a fiscal expansion.

Approach and positioning

We

remain flexible in our approach but are mindful of MMT risk and hence

remain very selective by company, and by country when we invest our

clients’ money. Living in the UK, having studied the Japanese experience

but investing in developed world bond markets, may not be a bad

position to assess the scene and provide sensible bond returns going

forwards.

Though forecasting is tricky, today we actually think US bond yields are cheap and, as real yields are positive, there is still capital to be made in US bond markets while that economy slowly turns Japanese. The UK and parts of Europe already have negative real yields (we are being repressed slowly). Our portfolios are barely exposed to UK corporate bonds for good reason and we prefer US corporate (and government) bonds as well as Australian sovereign bonds.

We invest thematically in a secular sense — you will get shorter term cyclical swings such as the two-year Trump reflation trade, which can confuse the narrative — but we continue to believe that most developed world bond yields are heading lower.

Glossary

- The Great Moderation: a period of economic stability characterised by low inflation, positive economic growth and the belief that the boom and bust cycles had been overcome. In the UK it generally refers to the period between 1993 and 2007.

- Financial repression: in simple terms, using regulations and policies to force down interest rates below the rate of inflation; also known as a ‘stealth tax’ that rewards debtors but punishes savers.

- Balance sheet recession: said to occur when high levels of private sector debt cause individuals and/or companies to focus on saving by paying down debt rather than spending or investing, which in turn results in slow economic growth or even decline. The term is attributed to the economist, Richard Koo.

- Secular stagnation: a prolonged period of low or no economic growth within an economy (excessive savings act as a drag on demand, reducing economic growth and inflation).

- Modern Monetary Theory (MMT): an unorthodox approach to economic management, which in simple terms argues that countries that issue their own currencies can ‘never run out of money’ the way people or businesses can. In other words, governments that have control of the monetary policy are not constrained by tax revenues for their spending. Developed in the 1990s, it has recently become a major topic of debate among US Democrats and economists.

- People’s quantitative easing: a policy proposed by the UK Labour Party leader, Jeremy Corbyn, which would require the Treasury (Debt Management Office) to create money to finance government investments on infrastructure via a public investment bank.

Diesen Beitrag teilen: