Columbia Threadneedle: China – bottom-up opportunity as the macro picture slowly improves

While the top-down story has challenges, the notion that China is ‘uninvestable’ is in our view misinformed. We believe company-specific opportunities can be found by looking at trade, value for money and capital return.

26.03.2024 | 07:20 Uhr

- While the top-down story has challenges, the notion that China is ‘uninvestable’ is in our view misinformed

- We believe that company-specific opportunities can be found by looking at trade, value for money and capital return

- Neither the US or China wants tensions to escalate, but the probability of a misstep/accident is not immaterial

Challenges faced by investors in China are well known, including property sector weakness, a lacklustre consumer environment and geopolitical tensions. In response, reports claiming that China is “uninvestable” have proliferated. We acknowledge the challenges but disagree with the assessment. Here are our current thoughts on these factors:

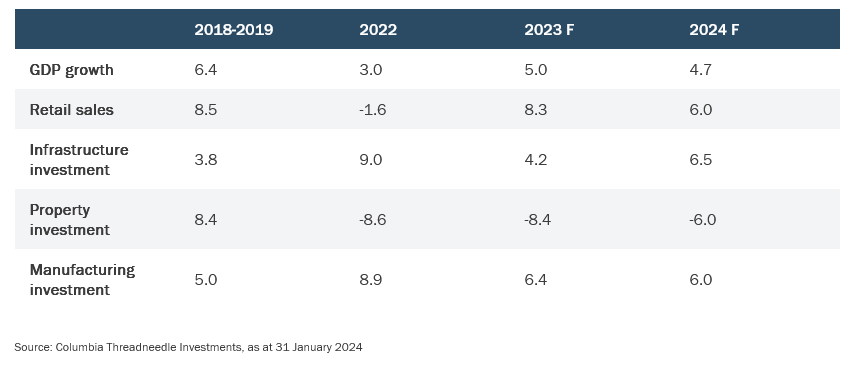

Property sector: Homebuyer trust remains weak amid developer defaults, and despite continual easing measures. Beijing and Shanghai cut downpayment ratios and mortgage rates for new borrowers in January. This followed a fall in tier 1 existing home prices by 1.4% month-on-month, the sharpest decline since 2011. Developer default risk also remains high as falling contract sales are negating government easing efforts.

Personal consumption: 2023 retail sales growth was comparable to pre-pandemic levels but was disappointing given the -1.6% growth we saw in 2022. In a post-pandemic world, consumption patterns have changed from: 1) things to lifestyle, 2) luxury to value, and 3) quality over quantity. Services consumption growth is expected to continue outperforming goods consumption in 2024. Medium-term consumption growth is expected to slow due to high underemployment. However, this may resolve as programs to address skill mismatches kick in, along with policies intended to promote higher consumption spending (eg, in education, housing and pensions).

Geopolitical tension: While frictions between the US and China have tactically eased, the underlying issues need to be addressed – particularly in relation to security, intellectual property, mercantilism and authoritarianism. Neither the US nor China wants a full-blown escalation, but the probability of a misstep/accident is not immaterial.

Beijing is seeking to offset some of these drags through investment. Infrastructure investment is expected to continue climbing in the first half of 2024 (Figure 1), highlighting the fast pace of government bond issuance that we saw in Q4 2023.

Figure 1: Infrastructure investment in China continues to accelerate (YoY change, %)

Manufacturing investment is expected to remain resilient as the government pushes to accelerate upgrades to manufacturing resources and the production of electric vehicles (EVs), batteries and renewables. While the top-down story has challenges, we think three themes are appealing:

Trade: With an $80 billion trade surplus, China is still a key global trading partner. It is worth noting that trade to other emerging market (EM) economies is increasing, which is plugging the hole created by supply chain diversification efforts. An example here is Chinese EV manufacturers, which are selling into economies such as Brazil and Indonesia. The weakening currency is working in favour of Chinese exporters.

Low cost/value for money: Providing consumers with value for money in a deflationary environment is important. Companies exposed to middle- and low-income consumers and those with strategic management are most attractive in this space – particularly companies competing with the likes of Alibaba and JD.com, as well as Amazon or even Dollar Stores.

Capital return: Given top-down uncertainty, investors will increasingly seek downside protection by identifying companies with low price-to-book ratios, increasing dividend yields and those undertaking stock buybacks. These can be powerful in a deflationary environment.

For investors to feel positive about China from a top-down perspective, the Xi government will need to fix the challenged property sector and restore business confidence domestically, all while projecting an aura of openness and peacefulness on the global stage. (Within the property sector in particular, it would be beneficial to see a clearing event, allowing troubled developers to go bust and remaining players to consolidate.)

We have witnessed green shoots, but they have often been pruned too early. For example, in 2023 we observed improving policy visibility, with announcements of state-owned enterprise reforms and the end of the regulatory cycle. This was cut short, however, by proposed rules to curb spending on video games, which wiped $80 billion off the value of Tencent and NetEase, both of which are widely owned blue-chip China stocks. (Confusion ensued when the announcement was swiftly reversed and the individual responsible at the regulator was dismissed.) This is a prime example of damage to both business and investor confidence, and we are seeing underinvestment by companies and a lack of corporate guidance as a result.

The government has shown it is prepared to provide stimulus, announcing an increase in the central deficit from 3% to 3.8%. This is a positive signal indicating a willingness to use the central government balance sheet instead of burdening local governments to stimulate growth. However, funds have been deployed in infrastructure and new manufacturing sectors and there is doubt that the government will use monies to address underlying issues. The recent banning of short selling and stock purchasing programs are testament to this.

Bottom line

While the macro challenges for China are formidable and will remain a focus for 2024, there are significant company-specific opportunities. The story is also optimistic for many of China’s EM trading partners. North Asian economies such as Korea and Taiwan are benefiting from the improvement in the semiconductor cycle, underpinned by AI demand and the smartphone replacement cycle. ASEAN economies such as Indonesia and Vietnam are witnessing demand for manufacturing capacity, which in turn will be a catalyst for urbanisation and consumption trends.

The main risks we see for the region and EM more generally are uncertainty from elections, the US Federal Reserve sustaining interest rates higher for longer, and geopolitical risk. More than 65% of the world’s population is facing an election in 2024, which could have a major impact on policy direction. However, the muted reaction from China following Lai Ching-te’s success in Taiwan is positive. We are still monitoring China’s posturing but Lai Ching-te has stated he will be pragmatic in working for independence.

Diesen Beitrag teilen: