In-Kind Transitions: A Primer

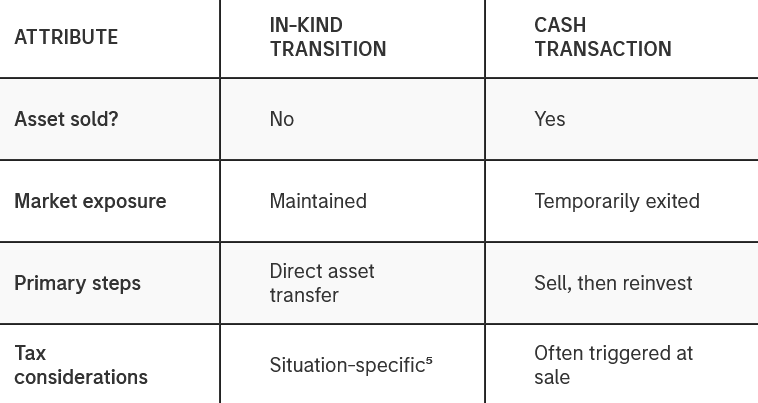

An in-kind transition refers to the transfer of an asset directly without selling it for cash.

09.04.2026 | 06:05 Uhr

Instead of liquidating a position and reinvesting the proceeds, the investor contributes or transfers the asset itself into a new structure or account, subject to eligibility and operational requirements. As a result, ownership of the underlying asset is generally maintained throughout the transition, even though the way the asset is held may change.¹

This approach differs from more traditional transitions, which typically involve selling the asset, temporarily holding cash and re-entering the market through a new investment.² Whether an in-kind transition is possible or appropriate depends on the specific asset, the destination structure and the investor’s individual circumstances.

Why In-Kind Transitions Matter

In-kind transitions can be relevant when investors want to change how an

asset is held—without changing what they own.

- MAINTAINING MARKET EXPOSURE Because the asset is not sold, exposure to the underlying investment is generally maintained during the transition, subject to operational timing and requirements.²

- REDUCING TRANSACTION COMPLEXITY An in-kind transition can eliminate multiple market transactions and the operational steps associated with selling and reinvesting, which may simplify execution in certain situations.¹

- POTENTIAL TAX CONSIDERATIONS Selling an asset for cash often triggers a taxable event. While tax treatment is highly fact-specific and depends on applicable law, in-kind transitions are sometimes evaluated as part of broader tax-aware planning discussions.³

- RELEVANCE FOR DIGITAL ASSETS Digital assets introduce additional considerations related to custody, trading venues and operational workflows. For investors who already hold digital assets, in-kind transitions may be explored as a way to reposition those holdings within a different investment or custody framework—without exiting and re-entering the market solely to change how the asset is held.⁴

How In-Kind Transitions Are Used

In-kind transitions are typically considered when an investor already owns

an asset and is evaluating whether a different structure, account type, or

investment vehicle may better align with their objectives. At a high level, the

process generally involves:

- Confirming that the asset is eligible for in-kind transfer¹

- Coordinating among custodians, counterparties, and administrators

- Transferring the asset directly into the new structure rather than selling it

Compared with a cash transaction, the distinction is straightforward.

Execution timelines, operational requirements and costs can vary, and in-kind transitions may take longer than standard market trades. As a result, they are typically planned in advance and coordinated with financial, tax and operational professionals.¹

What Kinds of Clients May Find In-Kind Transitions

Relevant?

In-kind transitions are not designed for every investor. They are

most often explored by clients who:

- Already hold meaningful positions in a specific asset

- Are evaluating changes to portfolio structure rather than asset exposure

- Have longer time horizons and less immediate liquidity needs

- Engage professional advisors as part of tax-aware or complex planning

- Are comfortable with additional operational coordination

These transitions are generally discussed in the context of broader portfolio construction and wealth-planning conversations rather than as standalone investment decisions. Suitability depends on an investor’s objectives, risk tolerance, liquidity needs and overall financial situation.

Key Takeaways

An in-kind transition is a method of transferring assets without converting

them to cash. For certain investors—particularly those with existing holdings

and complex planning needs—this approach may offer a way to reposition holdings

while generally maintaining exposure to the underlying asset.

Understanding how in-kind transitions work—and the considerations involved—can help investors and their advisors evaluate a broader set of tools when navigating portfolio and structural decisions.

Educational material only. Not a recommendation or solicitation.

1 Investment Company Institute (ICI), ETF Basics: The Creation and Redemption Process and Why It Matters (Jan. 19, 2012) — https://www.ici.org/viewpoints/view_12_etfbasics_creationrefresher-readings/2026/exchange-traded-funds-mechanics-applications

2 CFA Institute: Exchange Traded Funds—Mechanics and Applications (Curriculum/Refresher Reading) — https://www.cfainstitute.org/insights/professionallearning/

3 CFA Institute, Tax-Aware Investment Management (general reference on realized vs. unrealized gains) — https://www.cfainstitute.org/en/research/foundation/2015/tax-aware-investment-management

4 SEC Press Release: SEC Permits In-Kind Creations and Redemptions for Crypto ETPs (July 29, 2025) — https://www.sec.gov/newsroom/press-releases/2025-101-sec-permits-kind-creations-redemptions-crypto-etps

5 IRS: Digital assets (tax basics and reporting) — https://www.irs.gov/filing/digital-assets

For questions about in-kind transitions, please contact the MSIM ETF Specialist Team at etf_specialists@morganstanley.com.

RISK CONSIDERATIONS

Digital assets are highly volatile and unpredictable. Their value is

influenced by, but not limited to, supply and demand, investor confidence and

their willingness to purchase it using traditional currencies, inflation,

interest rates, currency exchange rates, changing regulations in the U.S. and

abroad, and economic trends. Investors also face risks such as price swings,

flash crashes, fraud, and cybersecurity threats. Digital assets may be more

vulnerable to market manipulation than securities.

Investing involves risk. Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Total Returns are calculated using the daily 4:00pm net asset value (NAV). Market price returns reflect the midpoint of the bid/ask spread as of the close of trading on the exchange where Fund shares are listed. Market price returns do not represent the returns you would receive if you traded shares at other times.

Diesen Beitrag teilen: