Quantitative Easing Has Begun: Is It Enough to Meaningfully Lower Mortgage Rates?

For over a quarter century, a well-known investment mantra – “Don’t Fight the Fed” – has advised investors to align their strategies with the prevailing monetary policy of the U.S. Federal Reserve

20.01.2026 | 05:00 Uhr

In other words, the Fed's influence on financial markets is so powerful that going against its direction is likely to result in losses. While that theory remains in play today, it is less relevant now as the Fed is less active in markets.

A new narrative for the markets has evolved over the past 12 months: don’t fight the U.S. presidential administration. Most recently, the administration has become more focused on the U.S. housing market and more specifically, ways to increase affordability, which is likely to be a 2026 mid-term election topic.

But how do you get more affordable housing? Two main factors contribute to housing affordability: financing cost (or mortgage rate) and the cost of the house itself. It’s unlikely the Trump administration wants existing home prices to tank, as that may topple existing homeowners. This puts focus on financing. To reduce financing costs, it helps to have tighter agency mortgage backed securities (MBS) spreads, and the bulk of newly created mortgages flow through Fannie Mae and Freddie Mac. It also helps to have lower Treasury yields, as most agency mortgages are fixed rate and priced off the Treasury curve, but that market is significantly larger and harder to manipulate. But what can the Trump administration do to achieve lower mortgage rates?

A Truth Social post late on Jan. 8 offered a potential roadmap, as President Trump posted: “I am instructing my representatives to BUY $200 Billion Dollars in Mortgage Bonds.” In this case, the groups doing the buying are the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac, which remain under government conservatorship. Mortgage rates dropped quickly, indicating significant market reaction and anticipated purchases, though the execution and pace of these large-scale purchases by the GSEs are still being clarified, impacting borrower affordability. Spreads instantly tightened 5-10 basis points (bps) on Fannie and Freddie bonds.

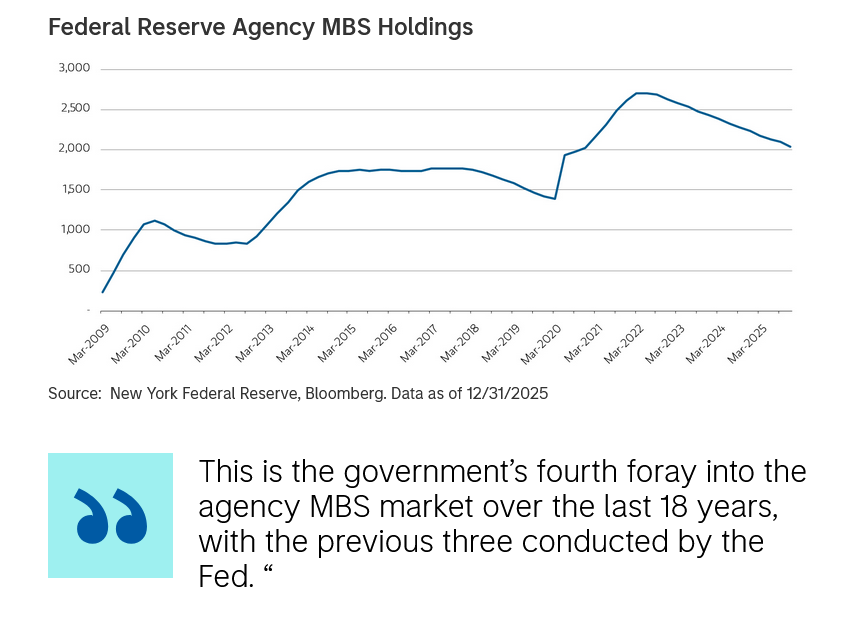

The agency MBS market, while not nearly as large as the Treasury market, is still over $9 trillion1, which means this purchase, once complete, makes up over 2% of the market. This is the government’s fourth foray into the agency MBS market over the last 18 years, with the previous three conducted by the Fed. Quantitative Easing (QE) 1, the Fed's first large-scale asset purchase program launched in late 2008 to combat the financial crisis, ended in 2010 and added $1.25 trillion in agency MBS to the Fed’s balance sheet. QE3, from 2012-2014, fattened the Fed’s balance sheet by roughly $1 trillion in agency MBS. QE4, launched in March 2020 during the COVID-19 pandemic to lower long-term rates and inject liquidity, bolstered the Fed’s balance sheet by $1.4 trillion in agency MBS over roughly two years.

While $200 billion in a $9 trillion-plus market2 may seem slight, there is another component to discuss. In markets, the flow part of the equation is much lower, with projections for net supply (or flow) somewhere in the range of $150-300 billion entering 20263, absent Fed runoff. Therefore, $200 billion in purchases would essentially be the supply for the year, which may have a big impact if Fannie and Freddie are programmatic buyers throughout the year like the Fed used to be.

One factor working against spreads is how the Fed’s agency MBS portfolio is likely to run off over the course of the year to the estimate of $200 billion, while Fannie and Freddie are buying $200 billion. So net government intervention is now potentially zero. Therefore, it stands to reason that net impact to the agency MBS market should then be zero. That’s false because the Fed’s runoff of $200 billion was already baked into agency MBS spreads, and this new buyer was not priced into the market, so now spreads have begun to recalibrate.

Bottom Line: The details of the Fannie and Freddie buying program remain elusive, and we are unlikely to get schedules like we used to see from the Fed’s previous buying programs. The Fed was a price insensitive buyer and remains still unclear how price sensitive Fannie and Freddie’s programs will be. However, Fannie and Freddie are unlikely to buy at any spread in the market, so the floor for agency MBS spreads is likely higher than previous government buying episodes. On the flipside, Fannie and Freddie will likely be there to help support any dips in the market. If spread out over the year, this program likely will accomplish its goal of tightening agency MBS spreads, but lower Treasury yields are needed to significantly lower mortgage rates, which will be based more around other macro factors like inflation and the labor market.

Fixed income securities are subject to the ability of an issuer to make timely principal and interest payments (credit risk), changes in interest rates (interest-rate risk), the creditworthiness of the issuer and general market liquidity (market risk). In a rising interest-rate environment, bond prices may fall and may result in periods of volatility and increased portfolio redemptions. In a declining interest-rate environment, the portfolio may generate less income. Longer-term securities may be more sensitive to interest rate changes. Mortgage and asset-backed securities are sensitive to early prepayment risk and a higher risk of default and may be hard to value and difficult to sell (liquidity risk). They are also subject to credit, market and interest-rate risks. Active management attempts to outperform a passive benchmark through proactive security selection and assumes considerable risk should managers incorrectly anticipate changing conditions.

There is no guarantee that any investment strategy will work under all market conditions, and each investor should evaluate their ability to invest for the long-term, especially during periods of downturn in the market.

A separately managed account may not be appropriate for all investors. Separate accounts managed according to the Strategy include a number of securities and will not necessarily track the performance of any index. Please consider the investment objectives, risks and fees of the Strategy carefully before investing. A minimum asset level is required.

Diesen Beitrag teilen: