Schroders: BoE - earlier and greater interest rate rises on the horizon

UK policymakers are concerned about inflation despite weak growth; we now forecast a November rate hike.

14.02.2018 | 09:46 Uhr

Following the latest Bank of England (BoE) press conference and publication of the quarterly Inflation Report, we are raising our forecast for the policy interest rate.

We now forecast a 25 basis point (bps) rate rise in November 2018, along with the two rate rises we had previously forecast for 2019.

Supply side constraints prompt our forecast change

The latest assessment from the BoE showed an upgrade to near-term growth dynamics, in part thanks to the better-than-expected GDP figures for Q4 2017, but also in part due to stronger growth in the rest of the world.

With regards to inflation, the near-term forecast was revised up substantially due to the rise in global oil prices over the past quarter.

However, the key factor which has prompted the change in our forecast was the updated assumptions from the BoE on the supply side of the economy.

The Bank has downgraded its estimate of potential growth from 1.7% to 1.5%, meaning even with its weak forecast for growth of between 1.7-1.8% over the coming years, it believes that spare capacity will be used up, and excess demand will appear by early 2020.

Hawkish comments from Carney

BoE Governor Mark Carney’s press conference was also notably more hawkish than usual. He ended his opening statement by saying that: “The MPC judges that, were the economy to evolve broadly in line with its February Inflation Report projections, monetary policy would need to be tightened somewhat earlier and by a somewhat greater extent over the forecast period than it anticipated at the time of the November Report, in order to return inflation sustainably to target.”

Of course, this statement contradicts the next part which was: “All members agree that any future increases in Bank Rate are expected to be gradual and to a limited extent”.

His comparison between the outlook today and that from November is unhelpful, as each is conditioned on different interest rate paths. For example, the inflation outlook for 2019 and 2020 is almost identical, though the latest forecast assumes three hikes over the next three years, compared to two back in November. That alone would warrant Carney’s statement, but when questioned more on rates this year, he refused to give any more clarity.

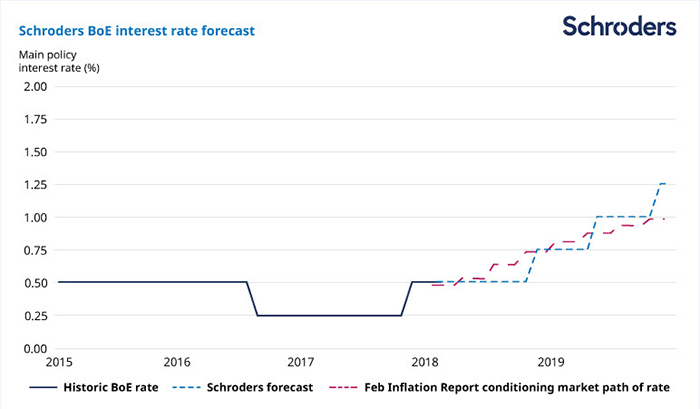

As shown by the below chart, our forecast will now be above the path on which the Bank has conditioned its latest forecast. We believe two elements from today’s communications suggest a more hawkish signal.

(Source: Bank of England February Inflation Report, Schroders Economics Group, 8 February 2018.)

First, the suggestion that excess demand could appear in 2020 should mean interest rates rising above the neutral rate (assumed to be around 2%) at the time. Alternatively, interest rates may rise back to the neutral rate more quickly, in order to head off overheating. The latter path tends to be preferred by central banks.

The second change in communication is that the Bank will now revert back to targeting inflation at the two-year horizon, rather than the extended three-year horizon it installed during the global financial crisis. In its inflation fan chart, the median/mean/modal path remains above 2% throughout the forecast, which suggests more restrictive policy is required.

Brexit impact still uncertain

As Carney said, the big uncertainty for the Bank’s forecast, and therefore path of policy rates, is Brexit. The Committee still expects a reasonably benign outcome for demand and supply, though the Bank’s downgrade of population and productivity forecasts is partly an acknowledgement of the impact of Brexit.

Die hierin geäußerten Ansichten und Meinungen stellen nicht notwendigerweise die in anderen Mitteilungen, Strategien oder Fonds von Schroders oder anderen Marktteilnehmern ausgedrückten oder aufgeführten Ansichten dar. Der Beitrag wurde am 09.02.18 auch auf schroders.com veröffentlicht.

Diesen Beitrag teilen: