NN IP: Spread markets resilient amid volatility, rising treasury yields

Spread markets have remained fairly resilient in the face of volatility and rising government bond yields. The solid macro background and unaltered monetary policy outlook are likely to remain key support factors for spread products.

19.02.2018 | 14:00 Uhr

Probably the most striking observation in financial markets so far this year has been the rise in government bond yields in developed markets. This rise has been more pronounced in the US and the UK and somewhat less so in the Eurozone. Japanese government bonds were practically unmoved, which affirms the maintained credibility of the BoJ’s yield curve targeting. Most of the action centred around a further market repricing of the Fed’s normalization path, continuing the trend started in September. This brought a corresponding rise in Treasury yields. A higher-than-anticipated average hourly earnings growth number in January’s US payroll data appeared to spook the market in this respect, fuelling a Phillips-curve type of rise in US inflation risks and lifting the term premium.

Spread markets also experienced some recent volatility, mainly in HY and EMD, but overall they have shown a fair degree of resilience since the start of the year. As was the case last year, spread performance so far this year has been more noteworthy in EUR credit paper than USD, including a solid tightening in Eurozone Peripheral spreads. Also like last year, the spread performance seen in EMD was more impressive in local currencies than in hard currencies.

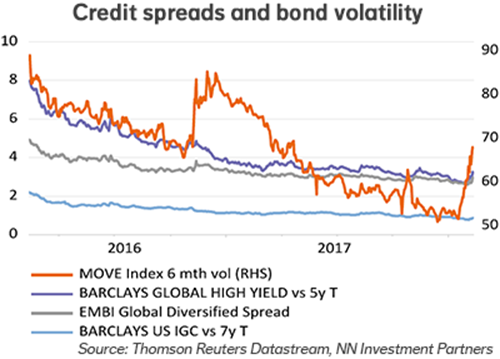

This year’s rise in government bond yields and bond market volatility has not been matched by a broad spread widening trend in spread products. This runs counter to the longer-term relationships between bond volatility, treasury yields and spread level direction that have existed in the past. Over longer periods, rising bond volatility has tended to lead to wider spreads across the board in spread products. Correlations between bond market volatility as expressed by the MOVE Index and spread levels of EMD LC, HC Sovereign, EUR and USD IG and global HY have been between +0.43 and +0.77 in the last decade. In the last three months or so, this correlation has reversed and moved into negative territory for the main spread categories, with a more pronounced year-to-date negative correlation exceeding -0.70 for EMD LC and EUR IG.

The same holds for spread correlation with 10 year US Treasury yields. So far this year and over the last three months, correlation is firmly negative almost across the board (higher Treasury yields – tighter spreads). This contradicts patterns seen over very long time periods, in which a negative correlation with US Treasury yields was mainly a phenomenon in IG space.

With the recent rise in bond market volatility not being matched by widening credit spreads, the debate has opened on whether a repricing in spreads is still due, particularly with spread product valuations being quite stretched almost across the board. Given the recent increased uncertainty, as expressed by the equity correction and simultaneous rise in bond market volatility, the valuation disconnect has not improved from that angle.

Macro background, gradual monetary normalisation will remain key supports

Nevertheless, we have seen similar periods of volatility in the past. Last year, periods of market tension that weighed on credit markets were ultimately overruled by the continuation of supportive fundamental forces. The two main supports for spread products are again likely to dominate this time – a continuation of solid, broad-based and synchronized macro data, and the outlook for a gradual path of the main central banks‘ policy normalization strategies.

The recent market tension centres around a surprise uptick in US wage inflation in January. Admittedly, this was a single data point that needs confirmation as to whether it marks the beginning of a trend. It is too early to tell, and our outlook for the Fed’s monetary policy exit has not changed. Market-based inflation expectations, moreover, have been rising recently in tandem with the rise in oil prices, which is currently fading. More importantly, the presence of slack in the Eurozone economy and a continued inflation undershoot still supports the case of a soft taper of the QE program by end-September. The BoJ’s expansionary monetary policy is also expected to continue. On this basis, spread product markets should still be supported in the near term and spreads could even tighten more.

Meanwhile, the rise in DM government bond yields in particular is starting to weigh on longer-duration and higher-rated credit paper, which will find it increasingly difficult to print positive total returns despite the current trend of spread tightening. This is already visible so far this year. Investment grade struggles to post positive returns; USD IG is already in negative territory. This is in contrast to the lower-duration and lower-rated spread products like HY and EMD LC. With investor flows tending to follow returns, IG may be disfavoured versus HY or EMD LC going forward.

In this environment, higher-beta categories of spread products may still be favoured. We are positioned accordingly, with IG neutral and USD HY overweight. We also hold an overweight in EMD LC (both rates and FX) to the detriment of EMD HC Sovereign, whose high duration is also a headwind.

Diesen Beitrag teilen: