Columbia Threadneedle: Chocks away! Airport passenger numbers – and financial metrics – recover

Increased numbers of fliers and supportive concession frameworks mean the industry retains a strong and steady credit trajectory.

28.03.2024 | 06:32 Uhr

Packing your bags and flying off to sunnier climes this Easter break? You’ll be joining the throng of travellers that contributed to airport passenger numbers exceeding pre-pandemic levels in the first months of 2024.

With the movement of people grinding to a halt during the Covid pandemic, it was an especially difficult period for airport operators. But financial metrics have recovered relatively swiftly from the tremendous drop in traffic.

This owes largely to strong operating models. Volume risk-sharing mechanisms provided support, while some tariffs shifted to annual resets and capex requirements were significantly reduced. This allowed for greater flexibility around uncertain traffic levels and hence cash preservation. Debt holders and shareholders also provided support through covenant waivers, capital injections and dividend pauses.

The pandemic also proved a useful litmus test as to how concession frameworks truly support credit quality in stressed environments. These vary widely across Europe. At the lightest-touch end of the spectrum, financial terms are directly negotiated with airlines and the airport shoulders all volume risk. This tends to be coupled with minimal oversight from a competition authority and private ownership.

At the highest-touch end, tariffs are dictated by a regulatory body which also requires specific levels of capex, typically with a degree of volume risk sharing.

Norwegian airport operator, Avinor, goes a step further. With full government ownership, airports in the country are clubbed together and regarded as a single unit, run to meet Norway’s connectivity needs and for greater sustainability and efficiency. This means profitable Norwegian airports – Oslo, for example – subsidise the operations of those that are loss making to ensure the populous remains connected across the country.

What does this mean for credit?

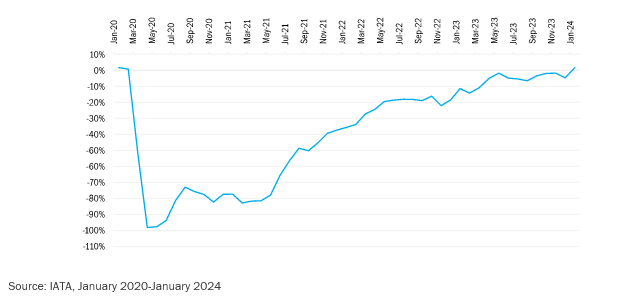

Airport operators received solid support through the pandemic. And, as mentioned, passenger numbers are now also recovering: through 2023 global traffic was only 6% below 2019 RPK (revenue passenger kilometre) levels. Europe had almost recovered to 2019 levels, only 5% below at FY23, with international recovery lagging domestic owing to China’s late reopening from Covid.1 Already in the first months of 2024 Europe has surpassed 2019 levels, with traffic up +1.5% in January (Figure 1).

Figure 1 European air passenger traffic versus 2019 levels (RPKs)

European passenger traffic growth is likely to continue – some European airports expect to exceed 2019 levels in 2024, others expect to take a couple more years to reach pre-pandemic traffic levels, but expect positive passenger growth nonetheless. In general, however, this is unlikely to lead to notable improvement in credit quality.

The benefit to revenue and profit from increased passenger numbers is balanced by higher cash outflows: capex levels are normalising and shareholder returns are being reinstated as the need for high conservativism has faded.

The strength of concession frameworks, and the fact that we view the credit trajectory as strong and steady, coupled with the typically long-dated nature of infrastructure bonds, makes the European airport sector attractive for investors such as insurers and pension funds looking for relatively stable, long-term positions.

And in a few cases we do see scope for credit improvement. Benefit from lagged tariff improvements or small revisions in regulatory frameworks should support further deleveraging at specific airports, including at Avinor and Schiphol, which are also at the higher-regulated, state-owned end of the spectrum, where we view credit quality as strongest.

1 IATA, January 2024

Diesen Beitrag teilen: