Henderson: Brexit - deal or no deal?

Paul O’Connor, Head of Multi-Asset, examines the implications of the UK triggering Article 50 of the Treaty of Lisbon, which formally begins the process of the UK’s withdrawal from the European Union (EU).

04.04.2017 | 10:15 Uhr

Prime Minister Theresa May has now triggered Article 50 of the Lisbon Treaty, officially starting the UK’s exit from the EU. The base case is that the UK will leave the EU by April 2019, giving two years to agree a divorce deal, future trading arrangements and a whole load of other practicalities. Since no member state has ever left the EU, there is no precedent for what lies ahead. What is clear, though, is that the initiative now shifts to the EU, which will dictate the rules and the timetable of the negotiations. A broad outline of these is expected to emerge shortly, although procedural requirements mean that the first formal face-to-face talks between the UK and the EU will probably not be held until late May or early June.

Time pressure

Time will be a key source of pressure throughout the negotiations. The various layers of ratification required to endorse the final agreement mean that talks will have to be completed by autumn 2018 – the effective negotiation period will therefore be much less than two years. Sequencing will be another key issue. While the UK government wants to negotiate the different elements of Brexit in parallel, the EU’s chief negotiator and some member states are demanding a divorce-first approach, delaying talks on a future trade deal until agreement has been reached on the UK’s exit bill, migrants’ rights and border issues with Ireland. While both sides could, in theory, agree to extend the deadline for talks, this option looks difficult given both political considerations in the UK and the fact that European Parliamentary elections are planned for May 2019.

Deal or no deal?

The process begins with few sharing the UK government’s optimism that a trade agreement can be reached within the timeframe allowed. The recently conducted trade deal between Canada and the EU took seven years to complete and that was conducted in a spirit of goodwill. The risk of a UK exit without a trade agreement is high. A no-deal, ‘hard Brexit’ outcome, with the UK falling back on World Trade Organization arrangements, would have a significantly adverse economic impact on the UK economy, by introducing tariff and non-tariff barriers to trade, disrupting supply chains and undermining the UK’s attractiveness as a location for foreign direct investment. It could also heighten political tensions in Northern Ireland and Scotland.

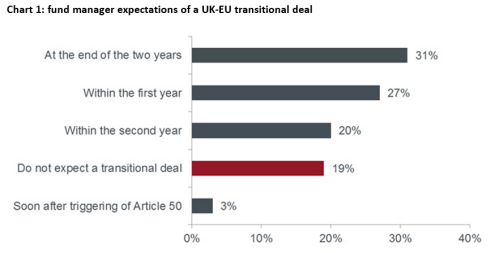

Even if one or both sides alter their negotiating stance, it is still hard to see how a final trade deal can be achieved in the time allotted. At this stage, the only plausible path to a softer outcome would seem to be if negotiations turned to establishing ‘transitional arrangements’. These could form a bridge from the end of the two-year period until some future time when a final trade-agreement could be in place. Survey evidence (chart 1) suggests that most asset managers believe that a transitional deal will emerge at some stage during the two-year period. We note, however, that the challenge is that any transitional arrangement would probably require the UK to retain many features of its current relationship with the EU, frustrating the government’s desire to implement some of its key Brexit objectives. The political cost might simply be too high. Significant political skill and compromise will be needed to steer away from a hard-Brexit in the narrow time-frame available.

Source: BoA Merrill Lynch. Note: Survey conducted 03-08 February 2017. Responses from UK, Continental Europe, Asia and US. Grey bars detail varying time period expectations for a transitional deal.

The wild card

One wild card to keep an eye on here is the case currently being presented to the Dublin courts, with the aim of ultimately getting the European Court of Justice to rule on whether Article 50 is revocable. While legal opinion is divided on the merits of this case, it could potentially have a significant bearing on the Brexit negotiations. If notification cannot be revoked, then Parliament will have little impact on the Brexit process from here, given that the final agreement will be presented on a take-it-or-leave-it basis. If however, the courts rule that Article 50 is revocable, the prospect of a Parliamentary rejection of the final deal becomes plausible and the possibility of a second referendum could, theoretically at least, be revived.

Diesen Beitrag teilen: