NN IP: Rotating into oil

Markets appear stable but some cyclical rotation is taking place below the surface. The main drivers are macro data, bond yields and oil prices. We upgrade energy from neutral to a small overweight.

02.10.2017 | 14:39 Uhr

Last week, all eyes were focused on Janet, Theresa and Angela, but none of them really surprised markets. The Fed is sticking to the game plan and will start reducing the balance sheet in October. Until the end of next year, four more rate hikes are indicated. This is more than we and the markets expect, so bond yields moved modestly higher in the US. May’s Brexit-speech in Florence did not reveal much more in the way of details, but it has become clearer that the UK is more clearly moving towards a soft Brexit and away from a hard or disruptive one.

Finally, the German elections were as expected, and only two coalitions are possible for Merkel’s CDU party to reach a majority – a coalition with the SPD, or a “Jamaican” coalition with the Greens and the FDP. As the SPD has signaled they want to move to the opposition side, only the Jamaican option is left to get a government with a parliamentary majority. It will not be an easy task for Merkel to find a compromise between the Greens and the Liberals and it may take some time, which is unusual in German politics. For Eurozone integration, this is not a good outcome. The impact on markets should be limited, however. Macroeconomic data in the Eurozone are very strong and should act as a counterweight.

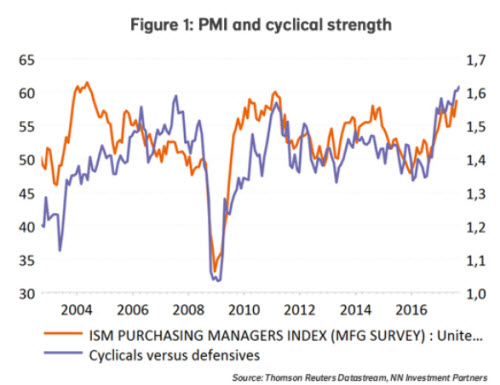

Over the week, global equities advanced a bit in euro terms. Below the surface we witnessed a modest comeback of the reflation trade. Financials outperformed and the bond-proxies lagged. The cyclical sectors also did well at the expense of health care and staples. We see three reasons behind this rotation. First of all is the strong macro data.

Second is the “hawkish” perception of the Fed. Historically, there exists a strong positive correlation between the trend in the Fed fund rate and the relative performance of cyclical sectors.

A third factor is the rise in the oil price impacting the relative performance of the energy sector.

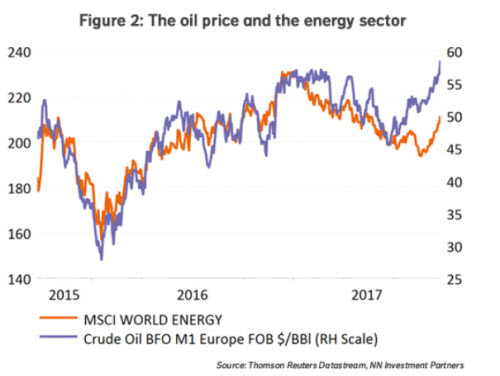

As a consequence, we upgraded the energy sector from neutral to a small overweight this week. Figure 2 shows that the sector has not followed the acceleration in the rise of the oil price. Even though the oil price has increased by 3% this year, the energy sector is still down year to date.

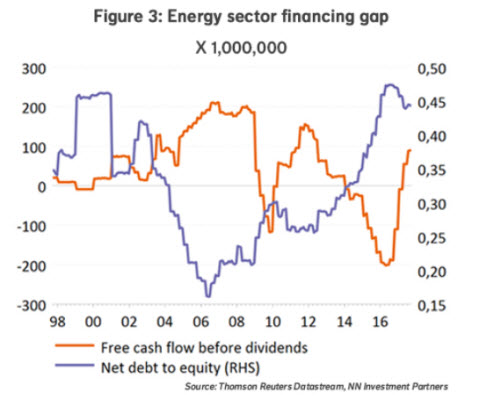

The oil price is of course the main determinant of the sector’s profitability. With oil above USD 50, the sector is certainly booking profits. This is also reflected in the earnings momentum, which is still negative but improving rapidly. At the same time, the free cash flow that is available to distribute dividends turned positive again and the net debt to equity ratio looks to have peaked.

Finally, positioning is low. According to the latest investor survey, the allocation to the sector has fallen to the lowest level since March 2016. A final remark relates to the importance of the sector for global earnings (representing over 12% over the past 20 years) and global capex (representing over 20% during 2012-2015).

Diesen Beitrag teilen: