Schroders: Energy price drop turns eurozone inflation negative

The preliminary estimate for eurozone HICP inflation shows annual price inflation has fallen into negative territory for the first time since October 2009.

07.01.2015 | 16:16 Uhr

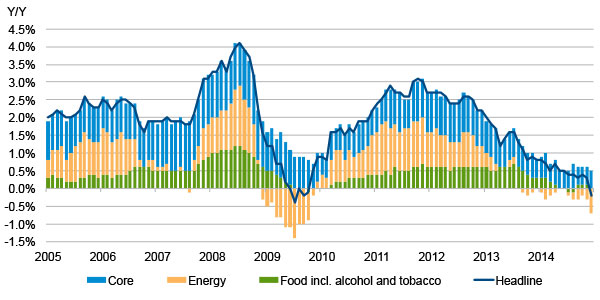

Inflation fell from 0.3% year-on-year (y/y) to -0.2% y/y in December, disappointing consensus expectations of -0.1% and raising fears that the eurozone is headed for a prolonged period of deflation. However, the details available so far show that the fall in inflation is being driven largely by external factors. When energy, food, alcohol & tobacco are excluded, the annual core inflation rate actually picked up from 0.7% to 0.8%.

The main driver of the drop in inflation has been the sharp fall in the energy sub-index. The price of European natural gas was hit at the start of 2014 due to unusually warm weather, while the recent collapse in global oil prices has also had a big downward impact.

Chart: Contribution to eurozone annual Harmonised Index of Consumer Prices (HICP) inflation rate

Source: Thomson Datastream, Eurostat, Schroders. 7 January 2015.

Deflationary fears are likely to remain high, and will probably increase pressure on the European Central Bank (ECB) to add further stimulus. However, there are few signs that the domestic European economy is becoming more deflationary. Consumer confidence remains reasonably high, while inflation expectations have not fallen to significantly low levels. Also, retail sales have held up well, suggesting households are not delaying spending in order to take advantage of falling prices. These are behavioural changes that are associated with the start of a prolonged deflationary period, like that experienced in Japan.

Domestically-driven inflation like the core rate (or even services inflation, which held up at 1.2% y/y) is low, but it does not signal deflation. Nevertheless, low headline inflation in itself increases the risk of deflation, as many administered prices domestically are linked to the headline rate. For example, following the fall in the headline rate into negative territory in 2006, the core inflation rate fell sharply about six months later. We could see this happen again later this summer. For this reason, we expect the ECB to change the composition of its asset purchases to include sovereign bonds in March, with a possible pre-announcement following the January meeting. The ECB may also choose to communicate a more ambitious purchasing target (larger balance sheet expansion), and may even look to accelerate the expansion of its balance sheet.

Diesen Beitrag teilen: