Henderson: US money / credit trends improving

A recent post argued that changes to US money market fund regulations in 2016 had a stifling impact on money and credit growth. The post suggested that this effect was starting to reverse, implying improving economic prospects for late 2017. Incoming evidence supports this hypothesis. The Fed may have to step up policy tightening to offset commercial bank-led monetary loosening.

24.05.2017 | 08:44 Uhr

(Foto: Simon Ward)

The regulatory changes resulted in money funds switching out of bank deposits and open market paper into Treasury and agency securities. The contention is that this portfolio shift boosted banks’ funding costs, leading them to reduce credit supply, causing a slowdown in money / lending and weaker spending. Money funds reduced their holdings of time deposits and open market paper by $583 billion during the last three quarters of 2016 while buying $431 billion of Treasury and agency securities, according to the Fed’s Z.1 financial accounts.

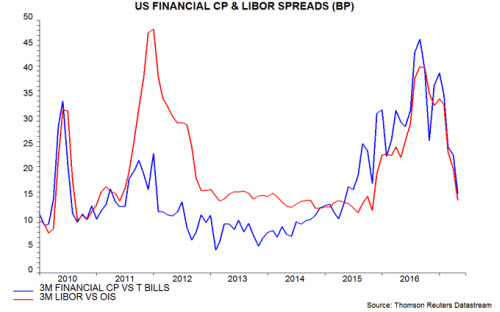

The yield spread between three-month financial commercial paper and Treasury bills rose from an average of 9 basis points (bp) in 2014 to a peak of 46 bp in September 2016 ahead of the October implementation of the new regulations. The spread, however, has fallen sharply in 2017, averaging 16 bp so far in May. The LIBOR / overnight indexed swap spread has behaved similarly – see first chart. This suggests that money funds had completed their portfolio adjustment by late 2016 and investment flows have normalised in 2017 (the Z.1 accounts for the first quarter will be released in early June).

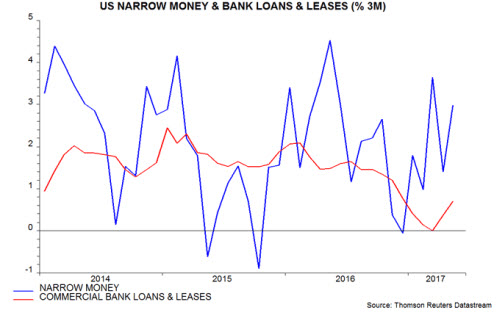

The fall in funding costs should, if the hypothesis is correct, boost credit supply and encourage spending. The latest money / lending data are consistent with this story. Three-month growth of narrow money has picked up from a low in December 2016, while three-month growth of commercial bank loans and leases appears to have bottomed in March – second chart*.

Bank credit tightening in 2016 capped economic strength, resulting in the Fed raising interest rates by less than expected. A reversal of the effect over the remainder of 2017 could require additional Fed tightening to prevent economic overheating. Such a scenario would suggest renewed upward pressure on Treasury yields and, possibly, the US dollar.

*Incorporates May estimates based on weekly data through 8-10 May.

Diesen Beitrag teilen: