Schroders: Where next for the value rally in Europe?

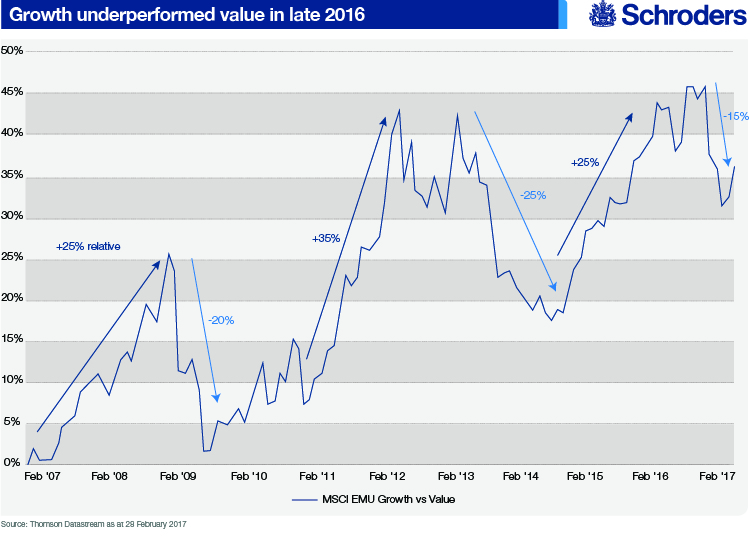

Eurozone equities enjoyed strong performance in the second half of 2016 as investors started to rotate towards value and higher risk areas of the market. Previously, investors had preferred to pay a premium for growth and quality stocks. That trend started to turn around in mid-2016 and picked up steam with the US elections.

13.03.2017 | 13:45 Uhr

Value rotation benefited banks

Bank stocks were among the chief beneficiaries of this rotation. The share prices of many banks had previously suffered due to low or negative interest rates, which put pressure on banks’ net interest margins. The prospect of rising inflation and higher interest rates therefore led the market to take a more positive view on banks.

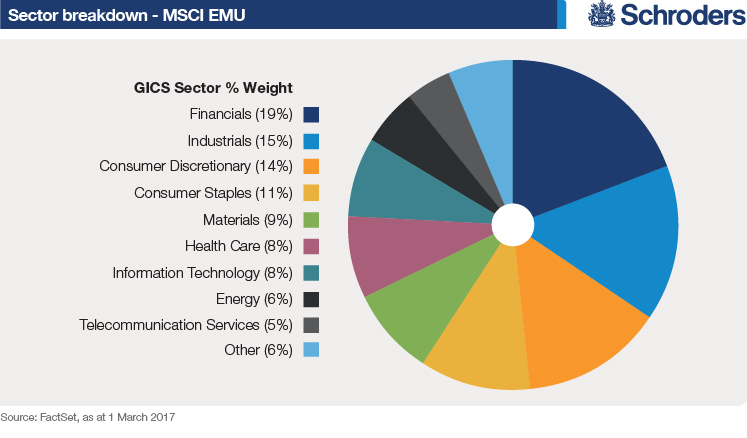

This helped to drive the overall eurozone market higher, since financials make up the largest individual sector in the MSCI EMU index. Other value and cyclical[4] sectors such as industrials and consumer discretionary (which includes automakers and retailers) are also well-represented.

Domestic listing, global reach

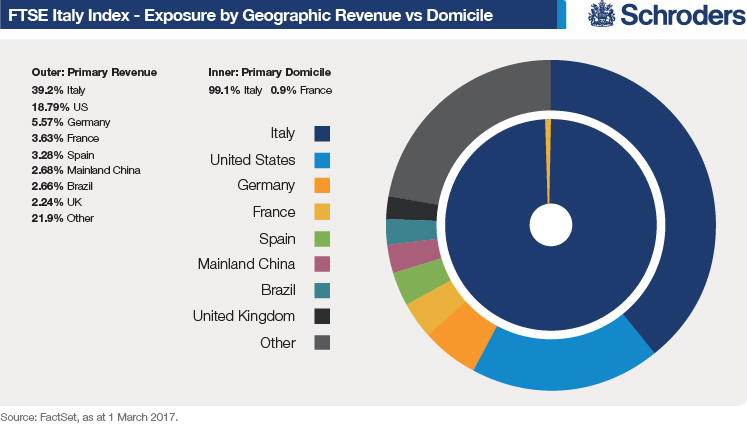

Italy is a market that we saw as an interesting source of value opportunities during 2016. The market came under pressure amid fears over the health of the banks and political uncertainty ahead of the constitutional referendum in December.

These worries depressed the share prices of companies that are domiciled in Italy but in fact have global operations. As the chart below indicates, while the vast majority of the index has its primary domicile in Italy, only 39% of revenues come from Italy.

Certainly there are a large number of banks in the index, many of which have entirely Italian-focused operations. However, alongside the household names in industries such as autos and luxury goods, the Italian index also contains some less well-known but still globally-exposed technology and industrial companies. The operational performance and growth opportunities for firms such as these are driven far more by global factors than domestic ones.

This is an important point with regard to the upcoming elections in several eurozone countries this year. Individual markets may be subject to volatility due to domestic political uncertainty. However, companies in those markets that have global reach could see little impact on their operations. This may throw up valuation anomalies that fundamental stockpickers such as ourselves are well-positioned to identify.

Can the value rally continue?

Overall, we feel it is not yet the moment to call time on the value trade. The macroeconomic environment looks supportive for value and higher risk stocks with rising inflation expectations around the world. This is good for corporates as it enables companies to raise prices, after years when prices were under pressure.

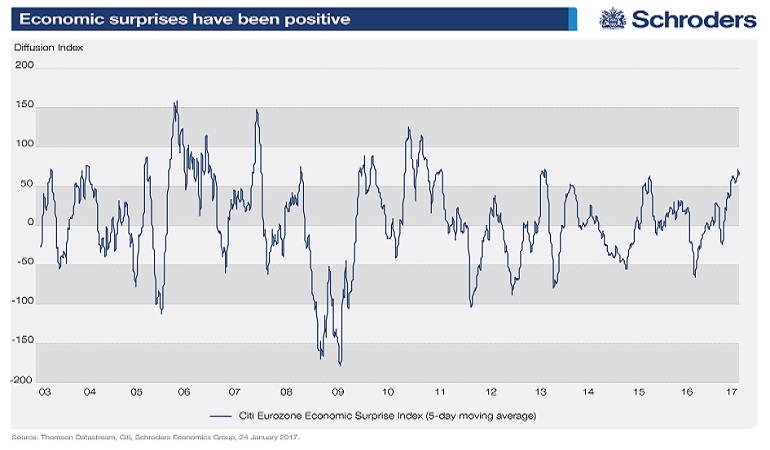

Indeed, the economic surprise index shows that macroeconomic data has been beating market expectations. This has particularly been the case in the US but is showing up in Europe too.

However, some caution is warranted. There is a danger of economic optimism becoming a consensus view, leading to a risk of disappointment if the data fails to carry on improving.

We must be mindful too of the risks around the eurozone’s upcoming elections. Indeed, we would have higher confidence in the continued longevity of the value rally in Europe if we could be sure of the outcomes of these.

Since that is impossible, we can draw some comfort from the 2016 examples of the Brexit vote, the US presidential election and the Italian referendum, where buying selected stocks on weakness around the votes proved a rewarding strategy.

Which sectors still represent value?

It is questionable whether banks represent value anymore following their rally. The sector is now a consensus call among investors. Many of the cheaper banks in Europe still face a sizeable burden of non-performing loans. There are few that are trading at reasonable valuations, generate capital, and do not face potentially significant litigation issues. We favour these higher quality banks but see few bargains in the sector.

The materials sector is one where we see some value opportunities presently. This is a cyclical area of the market so should benefit from the more robust economic backdrop. We note several industries, such as aluminium, are starting to see tighter supply which should result in rising prices.

Are defensive stocks now looking attractive?

We would highlight opportunities that can be found in those sectors left behind by the rotation towards value. Some of the more defensive sectors now look relatively more attractive.

For example, healthcare, which is a defensive and higher quality sector, has been largely out of favour. This has had as much to do with the US presidential election as the move towards higher risk stocks. The lack of clarity over the fate of the Affordable Care Act is denting sentiment. Markets dislike uncertainty, but there could be opportunities here once the picture clears.

Growth stocks are worth a mention too. We continue to like certain stocks within information technology which offer good potential for growth, especially where that is allied with cheap valuations.

Mergers and acquisitions can be another way of uncovering the value in a particular stock. Kraft Heinz’s approach for Unilever may have been swiftly withdrawn, but the fact it was considered at all shows that even consumer staples behemoths can be attractive bid targets.

Advantages of a blend approach

We would also highlight restructuring as another means by which many companies can unlock value within their businesses. We continue to look for restructuring potential in companies across sectors and styles.

Overall we now see more balanced prospects for value, growth and quality. The advantage for investors who take a blend approach is that we can consider ideas from any of these segments of the market, and avoid a heavy skew towards one segment in particular.

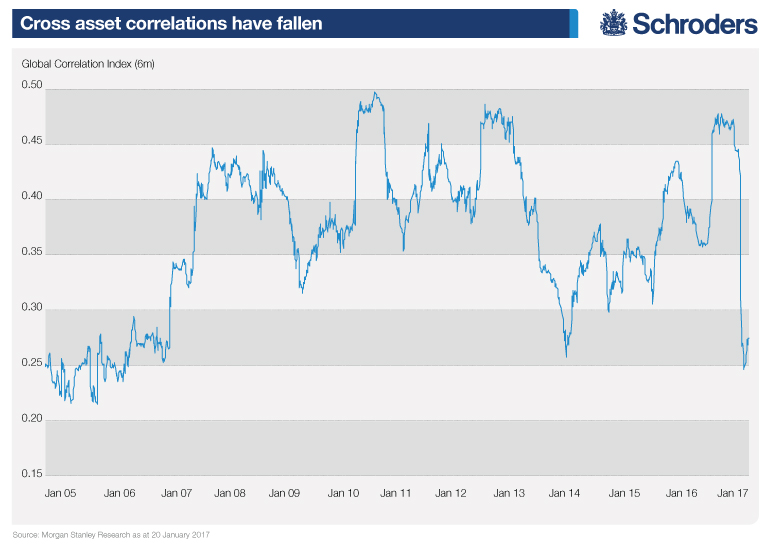

Above all, focusing on individual mispriced opportunities where we see a specific catalyst to improve operational and share price performance will continue to be our primary focus. With correlations between assets falling sharply recently, we feel this focus on individual stocks should prove successful.

Diesen Beitrag teilen: