Schroders: High beer prices could give investors a hangover

Increased competition, high valuations and the return of inflation could spell trouble for food & drink stocks.

10.10.2017 | 07:03 Uhr

When I first started going to pubs, a pint of beer cost around £2.00 and the choice was limited to three or four types, mostly well-known brand names. Now, beer costs around £5.00 a pint and it’s not unusual in London to see a selection of up to 30 different beers, most of which you’ve never heard of before.

This shows why high prices have not actually been good for the big beer companies. At £2.00 a pint they faced limited competition. At £5.00 a pint, start-up craft beer companies become financially viable and the market is flooded with new entrants.

Buying market share is costly

The situation is a catch-22 for the incumbent brewers: either lose market share to these insurgents or buy it back with what are potentially value-destructive mergers & acquisitions. In this world of cheap capital they tend to choose the latter. However, this leads to a bigger problem as it incentivises even more “have-a-go” entrepreneurs to try to create a competitor product.

This is a tough environment for the brewers to face and not a proposition that we find attractive as investors. What is more, the brewers and other consumer staples firms are currently trading on very expensive valuations.

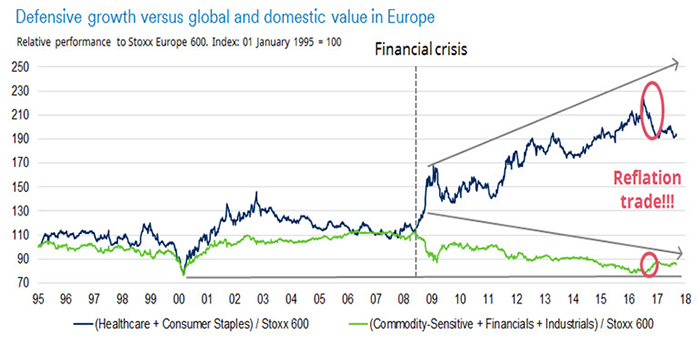

Defensives (1) have done well since financial crisis

In general, these consumer staples companies are well-run with stable revenues and consistent dividend payments. Such companies have been in high demand since the global financial crisis of 2008, with the result that they now look very expensive.

What is more, there are signs that the market backdrop that has persisted since the global financial crisis could soon change.

We had a taster of this last autumn when the “reflation trade”(2) saw a dip in the share prices of healthcare and staples stocks, while more economically-sensitive stocks gained. This is shown in the chart below, although it was only a small move.

Source: Kepler Cheuvreux, as at 9 August 2017. Past performance is not a guide to future performance and may not be repeated.

But we think the move last autumn was a practise run for what will happen in markets when inflation becomes more embedded. This could prove very painful for those so-called “sleep at night” defensive stocks currently sitting on lofty valuations.

Inflation poised for a comeback

Our view on the return of inflation is anti-consensual – many investors disagree with us and continue to favour those stocks that have done very well in the current environment. But we see signs that the backdrop is changing.

There are pockets of tightness in the labour market in Europe, putting upward pressure on wages in those areas. And capacity utilisation – a measure of how full factories are - is at high levels. This gives companies the option of either putting up prices or expanding to meet demand. Both of these are reflationary.

We should say here that we’re not expecting a huge move in inflation. Indeed, the market moves last autumn were prompted by inflation expectations moving from 1.3% to 1.8% which isn’t dramatic. But the market is pricing in a very extreme deflationary scenario, so any return to a “normal” environment could have a significant impact.

The return of inflation means investors will need a totally different portfolio from the one that has served them so well for the past few years. By the time this inflation shows up in the official CPI data, it will be too late. The market and asset prices will have already moved to reflect that.

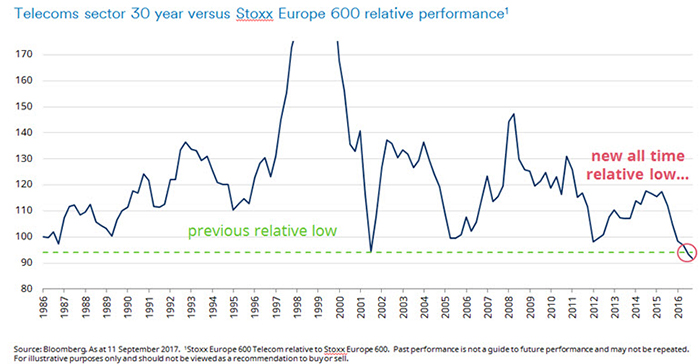

Banks and telcos benefit from inflation

Financials are among the chief beneficiaries of a pick-up in inflation. Bank stocks in particular are highly correlated with bond yields, meaning any pick-up in bond yields should benefit their profits and share prices.

The environment of falling bond yields and falling inflation has been terrible for telecoms stocks. They are hitting new all-time relative lows, which is a good starting point for a contrarian investor. At the same time, their fundamentals are brightening.

For the last five years, telcos have been investing very heavily but they are now starting to generate more cash. They’ve been building out 4G mobile networks and fibre to the home.

This is expensive to do, but once the fibre is there then that technology should be sufficient for households’ data needs for the next 30 years. When these investments are completed, in around three years’ time, these telco stocks should become cash-generating machines, in our view.

It’s the reverse situation to that facing the brewing stocks. Telecoms stocks trade on all-time low valuations and look poised to reap the rewards of past investment. Meanwhile, the brewers are expensively-valued and facing increasing competition.

(1) Defensive stocks provide a constant dividend and stable earnings regardless of the state of the overall stockmarket.

(2) The reflation trade refers to the ways prices may change if investors take the view that growth and inflation will rise.

Die hierin geäußerten Ansichten und Meinungen stellen nicht notwendigerweise die in anderen Mitteilungen, Strategien oder Fonds von Schroders oder anderen Marktteilnehmern ausgedrückten oder aufgeführten Ansichten dar.

Der Beitrag wurde am 09.10.17 auch auf schroders.com veröffentlicht.

Diesen Beitrag teilen: