Janus Henderson: Off the beaten path - US equities view

Gregory Kolb, Chief Investment Officer at Perkins, suggests following the approach of Charlie Munger, vice chairman of Berkshire Hathaway and Warren Buffett's longtime business partner. He did not ask how to generate X, but how to create non-X.

08.03.2018 | 12:10 Uhr

“I wish I knew where I was going to die, and then I’d never go there.” Charlie Munger, vice chairman of Berkshire Hathaway and Warren Buffett’s longtime business partner, has through the years used this notion to describe an approach to problem solving which he refers to as ‘inverting’ or addressing backward. That is to say, instead of asking how to create X, to turn the question around and ask how to create non-X*. Munger suggests that inverting in this manner is particularly useful when approaching hard problems.

“I wish I knew where I was going to die, and then I’d never go there.” Charlie Munger, vice chairman of Berkshire Hathaway and Warren Buffett’s longtime business partner, has through the years used this notion to describe an approach to problem solving which he refers to as ‘inverting’ or addressing backward. That is to say, instead of asking how to create X, to turn the question around and ask how to create non-X*. Munger suggests that inverting in this manner is particularly useful when approaching hard problems.

Let’s give it a try. Often, investors ask themselves “how can I achieve great returns?” That is a hard problem, that when inverted asks “How can I achieve non-great returns?” Or, if you prefer, “How can I achieve disastrous returns?” There are of course a variety of ways to achieve non-great returns. Purchasing stock in a company with an excessively leveraged balance sheet just prior to encountering operating difficulties is one example. Buying a firm facing escalating industry pressures but with no competitive moat to support it is another.

A third method of achieving non-great returns is particularly relevant today: overpaying for an asset. Both logic and experience are clear on this point. Pay too rich a valuation and returns will ultimately suffer. Investors would do well to recognise that global stocks are expensive, and that the US market in particular is at the second or third most expensive point in its long history. Therefore, not only is the forward return outlook modest, but the downside risk – should the market revert to a ‘merely average’ historical valuation – has rarely been greater. Amid the bullish excitement, many investors are seemingly forgetting to ask themselves, “How can I achieve disastrous returns?” and are simply buying into the extremely expensive US market via passive index funds and ETFs.

These vehicles by design will capture 100% of any downside that materializes in the years ahead, along with 100% of the upside, not accounting for fees. Significant drawdowns and the damage they inflict on portfolios, spending/retirement plans, etc, could be considered the financial equivalent of Munger’s “death,” and investors should carefully focus on never going there.

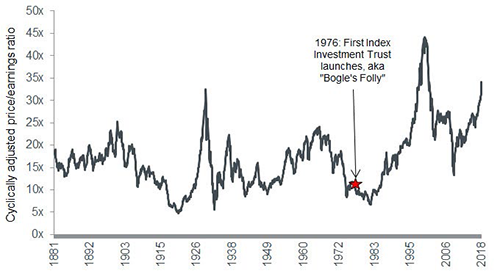

Cyclically adjusted price/earnings (P/E) ratio indicates expensive US market

(Source: http://www.econ.yale.edu/~shiller/data.htm, Vanguard, as at 31 January 2018.)

Notes: The cyclically adjusted P/E ratio is defined as price divided by the average of 10 years of earnings, adjusted for inflation. Data shown are for the S&P 500 Index.

Still, the exercise of considering what one should not do leaves one wanting more. A particular area of current interest is ‘off-the-beaten-path’ kinds of securities. We believe that less mainstream holdings may be less exposed to the general bullishness we observe, and crucially less exposed to any reversal in this level of bullishness. Our research efforts are increasingly focused on stocks with minimal Wall Street/sell-side analyst coverage, management teams that are not overly promotional, and niche businesses with secular business drivers. While the mainstream Las Vegas casino may be well known, perhaps the Korean counterpart is more obscure, and therefore potentially the better bargain. Instead of the well-known diversified chemical company benefiting from current/cyclical dynamics, consider the niche operator well positioned for structural trends, and so on. In navigating today’s great bull market, we believe that the further a stock is from the optimistic headlines, the better.

Extending this idea to portfolio construction, we favor an eclectic mix of holdings. Yes, there will be favoured sectors, such as consumer staples, and individual holdings that should be bought with conviction. However, in such an expensive and seemingly uncertain market environment, remember to diversify. A healthy mix of different drivers of alpha has the potential to strengthen portfolios. A well-constructed portfolio should be able to withstand a variety of news headlines and potential economic outcomes, and not just the positive ones. Ultimately, as the market and many of its individual stock components become increasingly unattractive from a risk/reward standpoint, we want any portfolio we manage to be less like the market.

Looking back, the beginning of index fund investing was timed quite well. When Jack Bogle launched the First Index Investment Trust (now the Vanguard 500 Index Fund) in August 1976, the cyclically adjusted price/earnings ratio (CAPE) was 11.6x. Bogle initially ‘bought’ well below the then long-term average CAPE of 15.1x, thus aiding his forward returns potential. Fast-forward to today and buyers of the original passive index fund are paying 34x earnings, which, as shown in the chart, is historically expensive.

We believe that today’s index fund buyers are, in a way, ignoring Munger’s sage advice about inverting when trying to solve the hard problems, forgetting to analyse what actions might lead to non-great returns. Instead, we suggest looking off the beaten path for stock ideas, and building eclectic portfolios. Careful consideration of downside risk, while attempting to position portfolios to reduce drawdown capture to well below 100%, are of paramount importance today.

* A transcript of Charlie’ Munger’s speech to the Harvard school, 13 June 1986 can be found by following this link: https://www.biznews.com/thought-leaders/1986/06/13/charlie-mungers-speech-to-the-harvard-school-june-1986/

Diesen Beitrag teilen: