Columbia Threadneedle: The Good, the Bad and the UK Stock Market

After an exceptional 2022 the UK stock market reverted to type, underperforming in 2023. With money continuing to disappear from the market, two potential catalysts for change have emerged.

02.04.2024 | 10:11 Uhr

- After an exceptional 2022, the UK reverted to recent type with a big underperformance in 2023, while the S&P and the eurozone hit all-time highs

- With money continuing to disappear from the UK market, two potential catalysts for change have emerged in the form of M&A and retail inflows

- We remain conviction investors who will look through the noise, avoid the whipsaw momentum trades and continue our deep and fundamental research to target strong, risk-adjusted returns

With global stock markets all about the Magnificent Seven1, investing in the UK over the past few years has been a little more The Good, The Bad and The Ugly. But what’s that on the horizon … it’s a bold new narrative riding into town!

Setting the scene

In 2022, with US tech reminding everybody that it can do cyclicality too, the UK stock market was the best performing developed market (The Good). Moving into 2023 brought worries over inflation and concerns about economic growth. The UK housing market and economy suffered from the impact of higher interest rates, more expensive mortgages and the subsequent hit to consumer spending that saw a sizeable pullback in spending on big ticket items (The Bad).

As we get further into 2024, however, perhaps we will sidestep The Ugly. The cost-of-living crisis is easing, the UK dallied with recession at the end of 2023 but looks to have immediately pulled out of it, and economic indicators are beginning to point in the right direction. So, while we’re not in a boom, or a High Noon period to extend the Western metaphor, we’re at least not worrying about how much further things could fall.

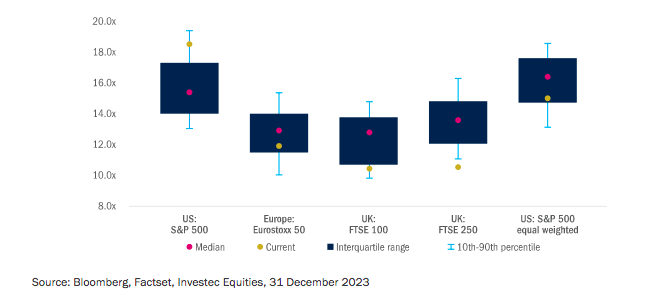

As 2023 came to a close the UK market found itself at 40-year lows against the S&P 500 and a 25-year low against the MSCI World Index (Figure 1).

Figure 1: UK equities appear cheap relative to their own history and to the rest of the world

So, if the general direction is up then what would be undeniably helpful would be to have money coming back to reinvest in listed shares. And there are two things which could be a positive catalyst for the UK market.

Catalyst one: M&A

First, the return of mergers and acquisitions (M&A), which effectively disappeared in 2023. As we have talked about many times, the FTSE 100 has lots of companies listed in it that don’t have anything to do with the UK economy, and their valuations are very low compared to their competitors. So it was a surprise that there was next to no M&A last year.

But there’s nothing like higher animal spirits for executive teams to take advantage of a situation. So in 2024, with debt markets continuing to reopen, we have already seen seven quite sizable bids including Virgin Money, Direct Line and DS Smith. All have been at least a 37% premium to the undisturbed share prices, and one or two have been spectacular.2 Wincanton, a little-known transport and logistics company which we hold in our portfolios, had a 104% premium. Telecoms testing services provider Spirent, meanwhile, was a 62% premium.3

Share prices got hit in 2023 on tougher trading, with investors caught up in the momentum and trajectory of short-term earnings and clustering around short positions or selling existing positions because shares were moving down. But we believe there is no information in share prices – it’s just a daily spot price that doesn’t necessarily tell you anything about the quality of the company, its long-term future returns or its intrinsic value as a business.

Below the radar of this daily noise of the flow trades of miners, banks and oils we think there is huge value in the UK. And what is coming through in this resumption of M&A activity is a reflection that the intrinsic value of these businesses is much higher than share prices are reflecting.

There is certainly a conversation to be had about declining numbers of listed companies in the UK, but today’s reality is that it is possible to get extremely strong returns from a market that has been written off, which is exciting.

Catalyst two: Budget bounce

In the recent Budget was a proposal for a British Individual Savings Account (ISA) of £5,000 per person.4 There are 800,000 people in the country that maximise their existing £20,000 ISA allowance.5 If they all take up the additional allocation that would be £4 billion coming into the market. In a £2 trillion market that is only 0.2%, but year-on-year compounding would be very helpful. The ISA is also a way of getting retail investors to look again at the UK stock market, which is crucial.

Also in the Budget was a proposal for the government to hold defined contribution and public sector pension schemes to account over their UK allocations, with the intention that “the government will review what further action should be taken if this data does not demonstrate that UK equity allocations are increasing.”6 The UK has hitherto been quite unusual in not enforcing this. In France and Italy, for example, you must hold a certain percentage of French and Italian equities, while in America you get tax benefits from investing in US-listed stocks.

Positioning ourselves

Although these things are not a silver bullet to turn the market around, they should be helpful. And whether we see this widespread mis-valuation of UK equities persist, or more money starts to flow back into the market, we believe our style of investing means we should benefit.

We remain patient, conviction investors. We have the grit, the True Grit (that’s the last Western mention, I promise!) to focus on the bottom-up, we do detailed, thorough research into company fundamentals and try to identify long-term value with a three- to five-year investment horizon. We stand back from the noise of the flow trades and the bulge bracket daily positioning. Buying equities involves long-term ownership and quality stewardship, and short-term losses will not fundamentally affect long-term intrinsic value. We will stay the course to see the strong, risk-adjusted returns realised.

1 Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. The mention of stocks is not a recommendation to deal

2 The last closing price before an offer announcement. Past performance is not a guide to future performance

3 RNS Newswire, March 2024. The mention of stocks is not a recommendation to deal

4 Gov.uk, Open Consultation UK Isa, 6 March 2024

5 AJ Bell, March 2024

6 Local Government Association, Spring Budget 2024: On-the-day briefing, 6 March 2024

Diesen Beitrag teilen: